Working with Market Depth and Trades

Display 3-depth

[1]:

from numba import njit

@njit

def print_3depth(hbt):

while hbt.elapse(60_000_000_000) == 0:

print('current_timestamp:', hbt.current_timestamp)

# Gets the market depth for the first asset, in the same order as when you created the backtest.

depth = hbt.depth(0)

# a key of bid_depth or ask_depth is price in ticks.

# (integer) price_tick = rice / tick_size

i = 0

for price_tick in range(depth.best_ask_tick, depth.best_ask_tick + 100):

qty = depth.ask_qty_at_tick(price_tick)

if qty > 0:

print(

'ask: ',

qty,

'@',

np.round(price_tick * depth.tick_size, 1)

)

i += 1

if i == 3:

break

i = 0

for price_tick in range(depth.best_bid_tick, max(depth.best_bid_tick - 100, 0), -1):

qty = depth.bid_qty_at_tick(price_tick)

if qty > 0:

print(

'bid: ',

qty,

'@',

np.round(price_tick * depth.tick_size, 1)

)

i += 1

if i == 3:

break

return True

[2]:

import numpy as np

btcusdt_20240809 = np.load('usdm/btcusdt_20240809.npz')['data']

btcusdt_20240808_eod = np.load('usdm/btcusdt_20240808_eod.npz')['data']

[3]:

from hftbacktest import BacktestAsset, HashMapMarketDepthBacktest

asset = (

BacktestAsset()

.data(btcusdt_20240809)

.initial_snapshot(btcusdt_20240808_eod)

.linear_asset(1.0)

.constant_latency(10_000_000, 10_000_000)

.risk_adverse_queue_model()

.no_partial_fill_exchange()

.trading_value_fee_model(0.0002, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

)

hbt = HashMapMarketDepthBacktest([asset])

print_3depth(hbt)

_ = hbt.close()

current_timestamp: 1723161661500000000

ask: 1.759 @ 61594.2

ask: 0.006 @ 61594.4

ask: 0.114 @ 61595.2

bid: 3.526 @ 61594.1

bid: 0.016 @ 61594.0

bid: 0.002 @ 61593.9

current_timestamp: 1723161721500000000

ask: 2.575 @ 61576.6

ask: 0.004 @ 61576.7

ask: 0.455 @ 61577.0

bid: 2.558 @ 61576.5

bid: 0.002 @ 61576.0

bid: 0.515 @ 61575.5

current_timestamp: 1723161781500000000

ask: 0.131 @ 61629.7

ask: 0.005 @ 61630.1

ask: 0.005 @ 61630.5

bid: 5.742 @ 61629.6

bid: 0.247 @ 61629.4

bid: 0.034 @ 61629.3

current_timestamp: 1723161841500000000

ask: 0.202 @ 61621.6

ask: 0.002 @ 61622.5

ask: 0.003 @ 61622.6

bid: 3.488 @ 61621.5

bid: 0.86 @ 61620.0

bid: 0.248 @ 61619.6

current_timestamp: 1723161901500000000

ask: 1.397 @ 61584.0

ask: 0.832 @ 61585.1

ask: 0.132 @ 61586.0

bid: 3.307 @ 61583.9

bid: 0.01 @ 61583.8

bid: 0.002 @ 61582.0

Efficient Market Depth Access

ROIVectorMarketDepth provides more efficient market depth access through a vector that holds a limited price range of interest. The backtester using this feature can be created by ROIVectorMarketDepthBacktest.

[4]:

from numba import njit

@njit

def print_3depth_fast(hbt):

roi_lb_tick = int(round(30000 / 0.1))

roi_ub_tick = int(round(90000 / 0.1))

while hbt.elapse(60_000_000_000) == 0:

print('current_timestamp:', hbt.current_timestamp)

# Gets the market depth for the first asset, in the same order as when you created the backtest.

depth = hbt.depth(0)

# a key of bid_depth or ask_depth is price in ticks.

# (integer) price_tick = price / tick_size

i = 0

for price_tick in range(depth.best_ask_tick, depth.best_ask_tick + 100):

# depth.ask_depth returns the ask depth array, whose length is (roi_ub_tick + 1 - roi_lb_tick),

# containing the quantities ranging from roi_lb_tick to roi_ub_tick.

# Checks that the price_tick is in that range and adjust the index by subtracting roi_lb_tick.

if price_tick < roi_lb_tick or price_tick > roi_ub_tick:

continue

t = price_tick - roi_lb_tick

qty = depth.ask_depth[t]

if qty > 0:

print(

'ask: ',

qty,

'@',

np.round(price_tick * depth.tick_size, 1)

)

i += 1

if i == 3:

break

i = 0

for price_tick in range(depth.best_bid_tick, max(depth.best_bid_tick - 100, 0), -1):

# depth.bid_depth returns the bid depth array, whose length is (roi_ub_tick + 1 - roi_lb_tick),

# containing the quantities ranging from roi_lb_tick to roi_ub_tick.

# Checks that the price_tick is in that range and adjust the index by subtracting roi_lb_tick.

if price_tick < roi_lb_tick or price_tick > roi_ub_tick:

continue

t = price_tick - roi_lb_tick

qty = depth.bid_depth[t]

if qty > 0:

print(

'bid: ',

qty,

'@',

np.round(price_tick * depth.tick_size, 1)

)

i += 1

if i == 3:

break

return True

[5]:

from hftbacktest import ROIVectorMarketDepthBacktest

asset = (

BacktestAsset()

.data(btcusdt_20240809)

.initial_snapshot(btcusdt_20240808_eod)

.linear_asset(1.0)

.constant_latency(10_000_000, 10_000_000)

.risk_adverse_queue_model()

.no_partial_fill_exchange()

.trading_value_fee_model(0.0002, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

# Sets the lower bound price for the range of interest in the market depth.

.roi_lb(30000)

# Sets the upper bound price for the range of interest in the market depth.

.roi_ub(90000)

)

[6]:

hbt = ROIVectorMarketDepthBacktest([asset])

print_3depth_fast(hbt)

_ = hbt.close()

current_timestamp: 1723161661500000000

ask: 1.759 @ 61594.2

ask: 0.006 @ 61594.4

ask: 0.114 @ 61595.2

bid: 3.526 @ 61594.1

bid: 0.016 @ 61594.0

bid: 0.002 @ 61593.9

current_timestamp: 1723161721500000000

ask: 2.575 @ 61576.6

ask: 0.004 @ 61576.7

ask: 0.455 @ 61577.0

bid: 2.558 @ 61576.5

bid: 0.002 @ 61576.0

bid: 0.515 @ 61575.5

current_timestamp: 1723161781500000000

ask: 0.131 @ 61629.7

ask: 0.005 @ 61630.1

ask: 0.005 @ 61630.5

bid: 5.742 @ 61629.6

bid: 0.247 @ 61629.4

bid: 0.034 @ 61629.3

current_timestamp: 1723161841500000000

ask: 0.202 @ 61621.6

ask: 0.002 @ 61622.5

ask: 0.003 @ 61622.6

bid: 3.488 @ 61621.5

bid: 0.86 @ 61620.0

bid: 0.248 @ 61619.6

current_timestamp: 1723161901500000000

ask: 1.397 @ 61584.0

ask: 0.832 @ 61585.1

ask: 0.132 @ 61586.0

bid: 3.307 @ 61583.9

bid: 0.01 @ 61583.8

bid: 0.002 @ 61582.0

Order Book Imbalance

[7]:

@njit

def orderbookimbalance(hbt, out):

roi_lb_tick = int(round(30000 / 0.1))

roi_ub_tick = int(round(90000 / 0.1))

while hbt.elapse(10 * 1e9) == 0:

depth = hbt.depth(0)

mid_price = (depth.best_bid + depth.best_ask) / 2.0

sum_ask_qty_50bp = 0.0

sum_ask_qty = 0.0

for price_tick in range(depth.best_ask_tick, roi_ub_tick + 1):

if price_tick < roi_lb_tick or price_tick > roi_ub_tick:

continue

t = price_tick - roi_lb_tick

ask_price = price_tick * depth.tick_size

depth_from_mid = (ask_price - mid_price) / mid_price

if depth_from_mid > 0.01:

break

sum_ask_qty += depth.ask_depth[t]

if depth_from_mid <= 0.005:

sum_ask_qty_50bp = sum_ask_qty

sum_bid_qty_50bp = 0.0

sum_bid_qty = 0.0

for price_tick in range(depth.best_bid_tick, roi_lb_tick - 1, -1):

if price_tick < roi_lb_tick or price_tick > roi_ub_tick:

continue

t = price_tick - roi_lb_tick

bid_price = price_tick * depth.tick_size

depth_from_mid = (mid_price - bid_price) / mid_price

if depth_from_mid > 0.01:

break

sum_bid_qty += depth.bid_depth[t]

if depth_from_mid <= 0.005:

sum_bid_qty_50bp = sum_bid_qty

imbalance_50bp = sum_bid_qty_50bp - sum_ask_qty_50bp

imbalance_1pct = sum_bid_qty - sum_ask_qty

imbalance_tob = depth.bid_depth[depth.best_bid_tick - roi_lb_tick] - depth.ask_depth[depth.best_ask_tick - roi_lb_tick]

out.append((hbt.current_timestamp, imbalance_tob, imbalance_50bp, imbalance_1pct))

return True

[8]:

from numba.typed import List

from numba.types import Tuple, float64

hbt = ROIVectorMarketDepthBacktest([asset])

tup_ty = Tuple((float64, float64, float64, float64))

out = List.empty_list(tup_ty, allocated=100_000)

orderbookimbalance(hbt, out)

_ = hbt.close()

[9]:

import polars as pl

df = pl.DataFrame(out).transpose()

df.columns = ['Local Timestamp', 'TOB Imbalance', '0.5% Imbalance', '1% Imbalance']

df = df.with_columns(

pl.from_epoch('Local Timestamp', time_unit='ns')

)

df

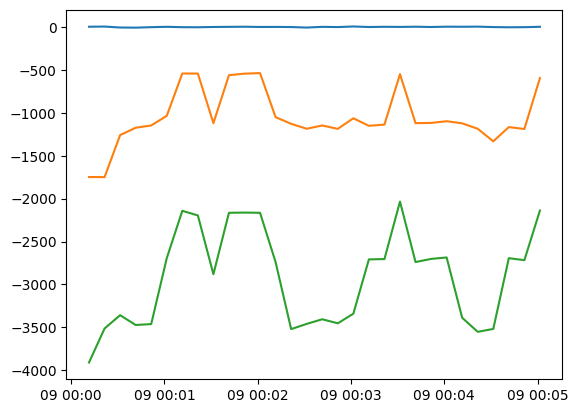

[9]:

shape: (30, 4)

| Local Timestamp | TOB Imbalance | 0.5% Imbalance | 1% Imbalance |

|---|---|---|---|

| datetime[ns] | f64 | f64 | f64 |

| 2024-08-09 00:00:11.500 | 2.729 | -1748.101 | -3908.736 |

| 2024-08-09 00:00:21.500 | 4.623 | -1749.435 | -3512.845 |

| 2024-08-09 00:00:31.500 | -6.465 | -1259.897 | -3357.755 |

| 2024-08-09 00:00:41.500 | -7.922 | -1174.185 | -3471.955 |

| 2024-08-09 00:00:51.500 | -2.484 | -1147.597 | -3461.48 |

| … | … | … | … |

| 2024-08-09 00:04:21.500 | 3.828 | -1186.236 | -3551.78 |

| 2024-08-09 00:04:31.500 | -1.35 | -1332.379 | -3517.854 |

| 2024-08-09 00:04:41.500 | -3.754 | -1166.521 | -2693.672 |

| 2024-08-09 00:04:51.500 | -2.525 | -1188.56 | -2716.914 |

| 2024-08-09 00:05:01.500 | 1.91 | -594.991 | -2138.82 |

[10]:

from matplotlib import pyplot

pyplot.plot(df['Local Timestamp'], df['TOB Imbalance'])

pyplot.plot(df['Local Timestamp'], df['0.5% Imbalance'])

pyplot.plot(df['Local Timestamp'], df['1% Imbalance'])

[10]:

[<matplotlib.lines.Line2D at 0x7f01eaf10520>]

Display last trades between the step

[11]:

from hftbacktest import BUY_EVENT

@njit

def print_trades(hbt):

while hbt.elapse(60 * 1e9) == 0:

print('-------------------------------------------------------------------------------')

print('current_timestamp:', hbt.current_timestamp)

# Gets the last trades occurring in the market, not the trades of our orders.

last_trades = hbt.last_trades(0)

num = 0

for last_trade in last_trades:

if num > 10:

print('...')

break

print(

'exch_timestamp:',

last_trade.exch_ts,

'buy' if (last_trade.ev & BUY_EVENT) == BUY_EVENT else 'sell',

last_trade.qty,

'@',

last_trade.px

)

num += 1

# To prevent accumulating all last trades, which may cause a slowdown,

# clear_last_trades needs to be called.

# After this, accessing `last_trades` will cause a crash.

hbt.clear_last_trades(0)

return True

[12]:

asset = (

BacktestAsset()

.data(btcusdt_20240809)

.initial_snapshot(btcusdt_20240808_eod)

.linear_asset(1.0)

.constant_latency(10_000_000, 10_000_000)

.risk_adverse_queue_model()

.no_partial_fill_exchange()

.trading_value_fee_model(0.0002, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

# To retrieve the last trades, `last_trades_capacity` should be set.

.last_trades_capacity(1000)

.roi_lb(30000)

.roi_ub(90000)

)

hbt = ROIVectorMarketDepthBacktest([asset])

print_trades(hbt)

_ = hbt.close()

-------------------------------------------------------------------------------

current_timestamp: 1723161661500000000

exch_timestamp: 1723161602372000000 buy 0.489 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.198 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.006 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.002 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.003 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.011 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.238 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.007 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.005 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.003 @ 61659.8

exch_timestamp: 1723161602372000000 buy 0.002 @ 61659.8

...

-------------------------------------------------------------------------------

current_timestamp: 1723161721500000000

exch_timestamp: 1723161661697000000 sell 0.002 @ 61594.1

exch_timestamp: 1723161661724000000 sell 0.002 @ 61594.1

exch_timestamp: 1723161661751000000 buy 0.135 @ 61594.2

exch_timestamp: 1723161661806000000 sell 1.328 @ 61594.1

exch_timestamp: 1723161661806000000 sell 0.002 @ 61594.1

exch_timestamp: 1723161661806000000 sell 0.002 @ 61594.1

exch_timestamp: 1723161661806000000 sell 0.002 @ 61594.1

exch_timestamp: 1723161661806000000 sell 0.006 @ 61594.1

exch_timestamp: 1723161661806000000 sell 0.32 @ 61594.1

exch_timestamp: 1723161661806000000 sell 0.032 @ 61594.1

exch_timestamp: 1723161661806000000 sell 1.208 @ 61594.1

...

-------------------------------------------------------------------------------

current_timestamp: 1723161781500000000

exch_timestamp: 1723161721541000000 sell 0.002 @ 61576.5

exch_timestamp: 1723161721574000000 buy 0.012 @ 61576.6

exch_timestamp: 1723161721578000000 sell 0.003 @ 61576.5

exch_timestamp: 1723161721583000000 buy 0.275 @ 61576.6

exch_timestamp: 1723161721583000000 buy 0.469 @ 61576.6

exch_timestamp: 1723161721585000000 buy 0.095 @ 61576.6

exch_timestamp: 1723161721585000000 buy 0.102 @ 61576.6

exch_timestamp: 1723161721585000000 buy 0.197 @ 61576.6

exch_timestamp: 1723161721586000000 buy 0.13 @ 61576.6

exch_timestamp: 1723161721587000000 buy 0.425 @ 61576.6

exch_timestamp: 1723161721587000000 buy 0.324 @ 61576.6

...

-------------------------------------------------------------------------------

current_timestamp: 1723161841500000000

exch_timestamp: 1723161781628000000 sell 0.026 @ 61629.6

exch_timestamp: 1723161781727000000 buy 0.011 @ 61629.7

exch_timestamp: 1723161781727000000 buy 0.05 @ 61629.7

exch_timestamp: 1723161781727000000 buy 0.006 @ 61629.7

exch_timestamp: 1723161781727000000 buy 0.002 @ 61629.7

exch_timestamp: 1723161781727000000 buy 0.007 @ 61629.7

exch_timestamp: 1723161781727000000 buy 0.002 @ 61629.7

exch_timestamp: 1723161781727000000 buy 0.075 @ 61629.7

exch_timestamp: 1723161781727000000 buy 0.065 @ 61629.7

exch_timestamp: 1723161781727000000 buy 0.247 @ 61629.7

exch_timestamp: 1723161781727000000 buy 0.002 @ 61629.7

...

-------------------------------------------------------------------------------

current_timestamp: 1723161901500000000

exch_timestamp: 1723161841561000000 buy 0.01 @ 61621.6

exch_timestamp: 1723161841561000000 buy 0.006 @ 61621.6

exch_timestamp: 1723161841561000000 buy 0.002 @ 61621.6

exch_timestamp: 1723161841561000000 buy 0.022 @ 61621.6

exch_timestamp: 1723161841561000000 buy 0.097 @ 61621.6

exch_timestamp: 1723161841561000000 buy 0.024 @ 61621.6

exch_timestamp: 1723161841564000000 buy 0.024 @ 61621.6

exch_timestamp: 1723161841564000000 buy 0.014 @ 61621.6

exch_timestamp: 1723161841565000000 buy 0.003 @ 61621.6

exch_timestamp: 1723161841613000000 buy 0.002 @ 61622.5

exch_timestamp: 1723161841613000000 buy 0.003 @ 61622.6

...

Rolling Volume-Weighted Average Price

[13]:

@njit

def rolling_vwap(hbt, out):

buy_amount_bin = np.zeros(100_000, np.float64)

buy_qty_bin = np.zeros(100_000, np.float64)

sell_amount_bin = np.zeros(100_000, np.float64)

sell_qty_bin = np.zeros(100_000, np.float64)

idx = 0

last_trade_price = np.nan

while hbt.elapse(10 * 1e9) == 0:

last_trades = hbt.last_trades(0)

for last_trade in last_trades:

if (last_trade.ev & BUY_EVENT) == BUY_EVENT:

buy_amount_bin[idx] += last_trade.px * last_trade.qty

buy_qty_bin[idx] += last_trade.qty

else:

sell_amount_bin[idx] += last_trade.px * last_trade.qty

sell_qty_bin[idx] += last_trade.qty

hbt.clear_last_trades(0)

idx += 1

if idx >= 1:

vwap10sec = np.divide(

buy_amount_bin[idx - 1] + sell_amount_bin[idx - 1],

buy_qty_bin[idx - 1] + sell_qty_bin[idx - 1]

)

else:

vwap10sec = np.nan

if idx >= 6:

vwap1m = np.divide(

np.sum(buy_amount_bin[idx - 6:idx]) + np.sum(sell_amount_bin[idx - 6:idx]),

np.sum(buy_qty_bin[idx - 6:idx]) + np.sum(sell_qty_bin[idx - 6:idx])

)

buy_vwap1m = np.divide(np.sum(buy_amount_bin[idx - 6:idx]), np.sum(buy_qty_bin[idx - 6:idx]))

sell_vwap1m = np.divide(np.sum(sell_amount_bin[idx - 6:idx]), np.sum(sell_qty_bin[idx - 6:idx]))

else:

vwap1m = np.nan

buy_vwap1m = np.nan

sell_vwap1m = np.nan

out.append((hbt.current_timestamp, vwap10sec, vwap1m, buy_vwap1m, sell_vwap1m))

return True

[14]:

hbt = ROIVectorMarketDepthBacktest([asset])

tup_ty = Tuple((float64, float64, float64, float64, float64))

out = List.empty_list(tup_ty, allocated=100_000)

rolling_vwap(hbt, out)

_ = hbt.close()

[15]:

df = pl.DataFrame(out).transpose()

df.columns = ['Local Timestamp', '10-sec VWAP', '1-min VWAP', '1-min Buy VWAP', '1-min Sell VWAP']

df = df.with_columns(

pl.from_epoch('Local Timestamp', time_unit='ns')

)

df

[15]:

shape: (30, 5)

| Local Timestamp | 10-sec VWAP | 1-min VWAP | 1-min Buy VWAP | 1-min Sell VWAP |

|---|---|---|---|---|

| datetime[ns] | f64 | f64 | f64 | f64 |

| 2024-08-09 00:00:11.500 | 61687.182976 | NaN | NaN | NaN |

| 2024-08-09 00:00:21.500 | 61709.337576 | NaN | NaN | NaN |

| 2024-08-09 00:00:31.500 | 61697.538054 | NaN | NaN | NaN |

| 2024-08-09 00:00:41.500 | 61663.958879 | NaN | NaN | NaN |

| 2024-08-09 00:00:51.500 | 61637.340621 | NaN | NaN | NaN |

| … | … | … | … | … |

| 2024-08-09 00:04:21.500 | 61643.009847 | 61624.459011 | 61626.495542 | 61622.549429 |

| 2024-08-09 00:04:31.500 | 61670.795685 | 61635.877251 | 61638.362314 | 61632.48854 |

| 2024-08-09 00:04:41.500 | 61643.108582 | 61641.846489 | 61648.672337 | 61636.032054 |

| 2024-08-09 00:04:51.500 | 61614.723569 | 61640.490841 | 61647.769844 | 61634.372128 |

| 2024-08-09 00:05:01.500 | 61584.697467 | 61637.334102 | 61642.209551 | 61632.12064 |

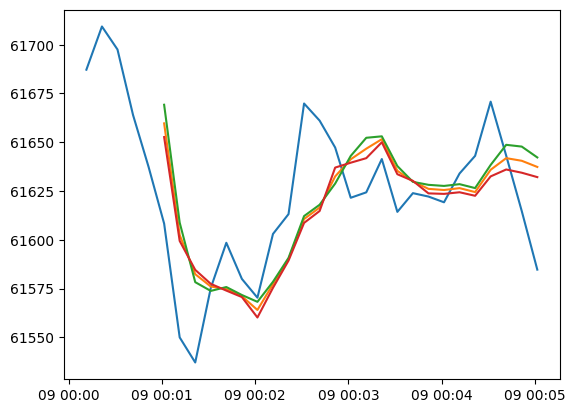

[16]:

pyplot.plot(df['Local Timestamp'], df['10-sec VWAP'])

pyplot.plot(df['Local Timestamp'], df['1-min VWAP'])

pyplot.plot(df['Local Timestamp'], df['1-min Buy VWAP'])

pyplot.plot(df['Local Timestamp'], df['1-min Sell VWAP'])

[16]:

[<matplotlib.lines.Line2D at 0x7f01b995e0b0>]