Order Fill

Exchange Models

HftBacktest is a market-data replay-based backtesting tool, which means your order cannot make any changes to the simulated market, no market impact is considered. Therefore, one of the most important assumptions is that your order is small enough not to make any market impact. In the end, you must test it in a live market with real market participants and adjust your backtesting based on the discrepancies between the backtesting results and the live outcomes.

Hftbacktest offers two types of exchange simulation. NoPartialFillExchange is the default exchange simulation where no partial fills occur. PartialFillExchange is the extended exchange simulation that accounts for partial fills in specific cases. Since the market-data replay-based backtesting cannot alter the market, some partial fill cases may still be unrealistic, such as taking market liquidity. This is because even if your order takes market liquidity, the replayed market data’s market depth and trades cannot change. It is essential to understand the underlying assumptions in each backtesting simulation.

NoPartialFillExchange

Conditions for Full Execution

Buy order in the order book

Your order price >= the best ask price

Your order price > sell trade price

Your order is at the front of the queue && your order price == sell trade price

Sell order in the order book

Your order price <= the best bid price

Your order price < buy trade price

Your order is at the front of the queue && your order price == buy trade price

Liquidity-Taking Order

Regardless of the quantity at the best, liquidity-taking orders will be fully executed at the best. Be aware that this may cause unrealistic fill simulations if you attempt to execute a large quantity.

You can find details below.

PartialFillExchange

Conditions for Full Execution

Buy order in the order book

Your order price >= the best ask price

Your order price > sell trade price

Sell order in the order book

Your order price <= the best bid price

Your order price < buy trade price

Conditions for Partial Execution

Buy order in the order book

Filled by (remaining) sell trade quantity: your order is at the front of the queue && your order price == sell trade price

Sell order in the order book

Filled by (remaining) buy trade quantity: your order is at the front of the queue && your order price == buy trade price

Liquidity-Taking Order

Liquidity-taking orders will be executed based on the quantity of the order book, even though the best price and quantity do not change due to your execution. Be aware that this may cause unrealistic fill simulations if you attempt to execute a large quantity.

You can find details below.

Queue Models

Knowing your order’s queue position is important to achieve accurate order fill simulation in backtesting depending on the liquidity of an order book and trading activities. If an exchange doesn’t provide Market-By-Order, you have to guess it by modeling. HftBacktest currently only supports Market-By-Price that is most crypto exchanges provide and it provides the following queue position models for order fill simulation.

Please refer to the details at Models <https://docs.rs/hftbacktest/latest/hftbacktest/backtest/models/index.html>.

RiskAverseQueueModel

This model is the most conservative model in terms of the chance of fill in the queue. The decrease in quantity by cancellation or modification in the order book happens only at the tail of the queue so your order queue position doesn’t change. The order queue position will be advanced only if a trade happens at the price.

You can find details below.

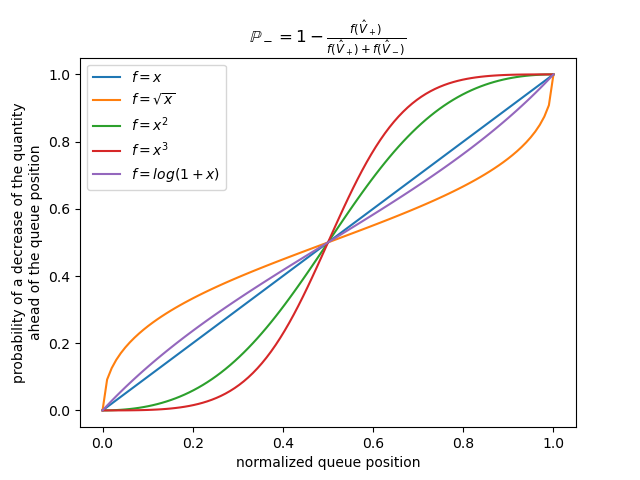

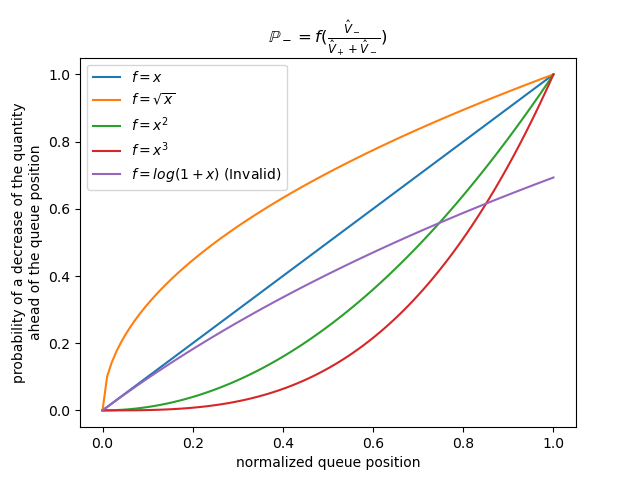

ProbQueueModel

Based on a probability model according to your current queue position, the decrease in quantity happens at both before and after the queue position. So your queue position is also advanced according to the probability. This model is implemented as described in

You can find details below.

By default, three variations are provided. These three models have different probability profiles.

The function f = log(1 + x) exhibits a different probability profile depending on the total quantity at the price level, unlike power functions.

When you set the function f, it should be as follows.

The probability at 0 should be 0 because if the order is at the head of the queue, all decreases should happen after the order.

The probability at 1 should be 1 because if the order is at the tail of the queue, all decreases should happen before the order.

You can see the comparison of the models here.

Implement a custom queue model

You need to implement the following traits in Rust based on your usage requirements.

Please refer to the queue model implementation.

References

This is initially implemented as described in the following articles.