Market Making with Alpha - Order Book Imbalance

Overview

Order Book Imbalance, also known as Order Flow Imbalance, is a widely recognized microstructure indicator often analyzed alongside trade flow. This concept has several derivatives, including the Micro-Price, VAMP (Volume Adjusted Mid Price), Weighted-Depth Order Book Price, and Static Order Book Imbalance, among others.

Static Order Book Imbalance

\[Static\ Order\ Book\ Imbalance = {\sum_{i}^N{Q_{bid}^i - \sum_{i}^N{Q_{ask}^i}} \over {\sum_{i}^NQ_{bid}^i + \sum_{i}^NQ_{ask}^i}}\]- Volume Adjusted Mid PriceBe aware that price and quantity are cross-multiplied between bid and ask sides.\[VAMP_{bbo} = {P_{best\ bid} \times Q_{best\ ask} + P_{best\ ask} \times Q_{best\ bid} \over {Q_{best\ bid} + Q_{best\ ask}}}\]\[VAMP_N = {\sum_{i}^N{P_{bid}^i \times Q_{ask}^i} + \sum_{i}^N{P_{ask}^i \times Q_{bid}^i} \over {\sum_{i}^NQ_{bid}^i + \sum_{i}^NQ_{ask}^i}}\]

where N is usually defined as a percentage of the mid price. For 1% market depth, compute bid side down to mid × 0.99 and ask side up to mid × 1.01.

- Weighted-Depth Order Book PriceBe aware that price and quantity are multiplied within the same side\[Weighted-Depth\ Order\ Book\ Price = {\sum_{i}^N{P_{bid}^i \times Q_{bid}^i} + \sum_{i}^N{P_{ask}^i \times Q_{ask}^i} \over {\sum_{i}^NQ_{bid}^i + \sum_{i}^NQ_{ask}^i}}\]

In this case, N—unlike in VAMP—is defined by a fixed total quantity. For 500 qty of market depth, compute bid side down to its total quantity reachs 500 and ask side up to its total quantity reachs 500. Alternatively, you can use notional value instead of quantity.

Another variation is to combine VAMP with Weighted-Depth Order Book Price.

\[P_{effective\ bid}^N = {\sum_{i}^N{P_{bid}^i \times Q_{bid}^i} \over {\sum_{i}^NQ_{bid}^i}}\]\[P_{effective\ ask}^N = {\sum_{i}^N{P_{ask}^i \times Q_{ask}^i} \over {\sum_{i}^NQ_{ask}^i}}\]\[Q_{effective\ bid}^N = \sum_{i}^NQ_{bid}^i\]\[Q_{effective\ ask}^N = \sum_{i}^NQ_{ask}^i\]\[VAMP_N = {{P_{effective\ bid}^N \times Q_{effective\ ask}^N + P_{effective\ ask}^N \times Q_{effective\ bid}^N} \over {Q_{effective\ bid}^N + Q_{effective\ ask}^N}}\]where N is defined just like VAMP.

These derivatives may also undergo statistical adjustments, such as standardization. Extensive information is available online regarding these indicators. In the examples that follow, we will these indicators.

Reference

Note: This example is for educational purposes only and demonstrates effective strategies for high-frequency market-making schemes. All backtests are based on a 0.005% rebate, the highest market maker rebate available on Binance Futures. See Binance Upgrades USDⓢ-Margined Futures Liquidity Provider Program for more details.

[1]:

import numpy as np

from numba import njit, uint64

from numba.typed import Dict

from hftbacktest import (

BacktestAsset,

ROIVectorMarketDepthBacktest,

GTX,

LIMIT,

BUY,

SELL,

BUY_EVENT,

SELL_EVENT,

Recorder

)

from hftbacktest.stats import LinearAssetRecord

@njit

def obi_mm(

hbt,

stat,

half_spread,

skew,

c1,

looking_depth,

interval,

window,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

):

asset_no = 0

imbalance_timeseries = np.full(30_000_000, np.nan, np.float64)

tick_size = hbt.depth(0).tick_size

lot_size = hbt.depth(0).lot_size

t = 0

roi_lb_tick = int(round(roi_lb / tick_size))

roi_ub_tick = int(round(roi_ub / tick_size))

while hbt.elapse(interval) == 0:

hbt.clear_inactive_orders(asset_no)

depth = hbt.depth(asset_no)

position = hbt.position(asset_no)

orders = hbt.orders(asset_no)

best_bid = depth.best_bid

best_ask = depth.best_ask

mid_price = (best_bid + best_ask) / 2.0

sum_ask_qty = 0.0

from_tick = max(depth.best_ask_tick, roi_lb_tick)

upto_tick = min(int(np.floor(mid_price * (1 + looking_depth) / tick_size)), roi_ub_tick)

for price_tick in range(from_tick, upto_tick):

sum_ask_qty += depth.ask_depth[price_tick - roi_lb_tick]

sum_bid_qty = 0.0

from_tick = min(depth.best_bid_tick, roi_ub_tick)

upto_tick = max(int(np.ceil(mid_price * (1 - looking_depth) / tick_size)), roi_lb_tick)

for price_tick in range(from_tick, upto_tick, -1):

sum_bid_qty += depth.bid_depth[price_tick - roi_lb_tick]

imbalance_timeseries[t] = sum_bid_qty - sum_ask_qty

# Standardizes the order book imbalance timeseries for a given window

m = np.nanmean(imbalance_timeseries[max(0, t + 1 - window):t + 1])

s = np.nanstd(imbalance_timeseries[max(0, t + 1 - window):t + 1])

alpha = np.divide(imbalance_timeseries[t] - m, s)

#--------------------------------------------------------

# Computes bid price and ask price.

order_qty = max(round((order_qty_dollar / mid_price) / lot_size) * lot_size, lot_size)

fair_price = mid_price + c1 * alpha

normalized_position = position / order_qty

reservation_price = fair_price - skew * normalized_position

bid_price = min(np.round(reservation_price - half_spread), best_bid)

ask_price = max(np.round(reservation_price + half_spread), best_ask)

bid_price = np.floor(bid_price / tick_size) * tick_size

ask_price = np.ceil(ask_price / tick_size) * tick_size

#--------------------------------------------------------

# Updates quotes.

# Creates a new grid for buy orders.

new_bid_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price < max_position_dollar and np.isfinite(bid_price):

for i in range(grid_num):

bid_price_tick = round(bid_price / tick_size)

# order price in tick is used as order id.

new_bid_orders[uint64(bid_price_tick)] = bid_price

bid_price -= grid_interval

# Creates a new grid for sell orders.

new_ask_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price > -max_position_dollar and np.isfinite(ask_price):

for i in range(grid_num):

ask_price_tick = round(ask_price / tick_size)

# order price in tick is used as order id.

new_ask_orders[uint64(ask_price_tick)] = ask_price

ask_price += grid_interval

order_values = orders.values();

while order_values.has_next():

order = order_values.get()

# Cancels if a working order is not in the new grid.

if order.cancellable:

if (

(order.side == BUY and order.order_id not in new_bid_orders)

or (order.side == SELL and order.order_id not in new_ask_orders)

):

hbt.cancel(asset_no, order.order_id, False)

for order_id, order_price in new_bid_orders.items():

# Posts a new buy order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_buy_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

for order_id, order_price in new_ask_orders.items():

# Posts a new sell order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_sell_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

t += 1

if t >= len(imbalance_timeseries):

raise Exception

# Records the current state for stat calculation.

stat.record(hbt)

[2]:

%%time

roi_lb = 10000

roi_ub = 50000

latency_data = np.concatenate(

[np.load('latency/live_order_latency_{}.npz'.format(date))['data'] for date in range(20230501, 20230532)]

)

asset = (

BacktestAsset()

.data(['data2/btcusdt_{}.npz'.format(date) for date in range(20230501, 20230532)])

.initial_snapshot('data2/btcusdt_20230430_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(2)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 30_000_000)

half_spread = 80

skew = 3.5

c1 = 160

depth = 0.025 # 2.5% from the mid price

interval = 1_000_000_000 # 1s

window = 3_600_000_000_000 / interval # 1hour

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 50

grid_num = 1

grid_interval = hbt.depth(0).tick_size

obi_mm(

hbt,

recorder.recorder,

half_spread,

skew,

c1,

depth,

interval,

window,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/obi_btcusdt.npz')

CPU times: user 32min 23s, sys: 43.9 s, total: 33min 7s

Wall time: 33min 5s

[3]:

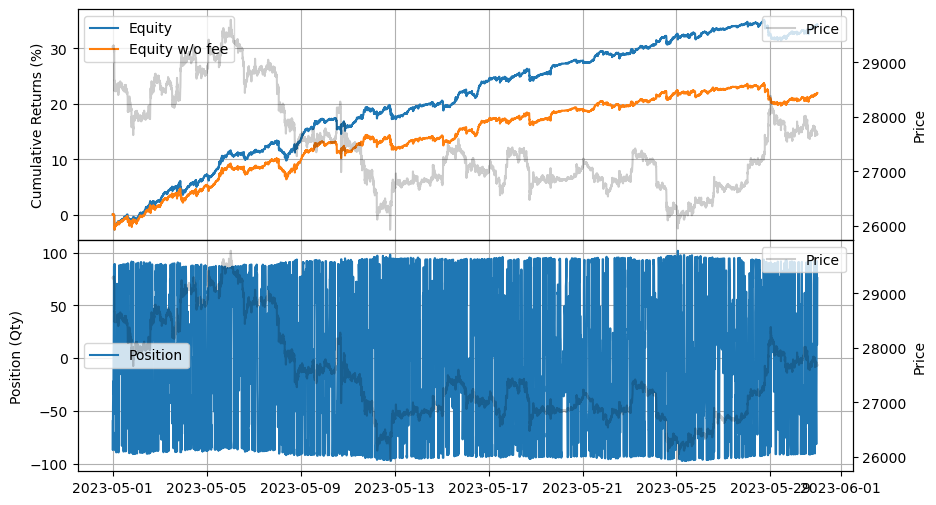

data = np.load('stats/obi_btcusdt.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

[3]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2023-05-01 00:00:00 | 2023-05-30 23:55:00 | 10.829336 | 13.5994 | 0.342371 | 0.037249 | 4119.876838 | 82.397448 | 9.191522 | 0.000139 | 2.6383e6 |

[4]:

stats.plot()

[5]:

%%time

roi_lb = 0

roi_ub = 3000

latency_data = np.concatenate(

[np.load('latency/live_order_latency_{}.npz'.format(date))['data'] for date in range(20230501, 20230532)]

)

asset = (

BacktestAsset()

.data(['data2/ethusdt_{}.npz'.format(date) for date in range(20230501, 20230532)])

.initial_snapshot('data2/ethusdt_20230430_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(2)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.01)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 30_000_000)

half_spread = 5

skew = 0.2

c1 = 10

depth = 0.025 # 2.5% from the mid price

interval = 1_000_000_000 # 1s

window = 3_600_000_000_000 / interval # 1hour

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 50

grid_num = 1

grid_interval = hbt.depth(0).tick_size

obi_mm(

hbt,

recorder.recorder,

half_spread,

skew,

c1,

depth,

interval,

window,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/obi_ethusdt.npz')

CPU times: user 27min 37s, sys: 38.3 s, total: 28min 15s

Wall time: 28min 16s

[6]:

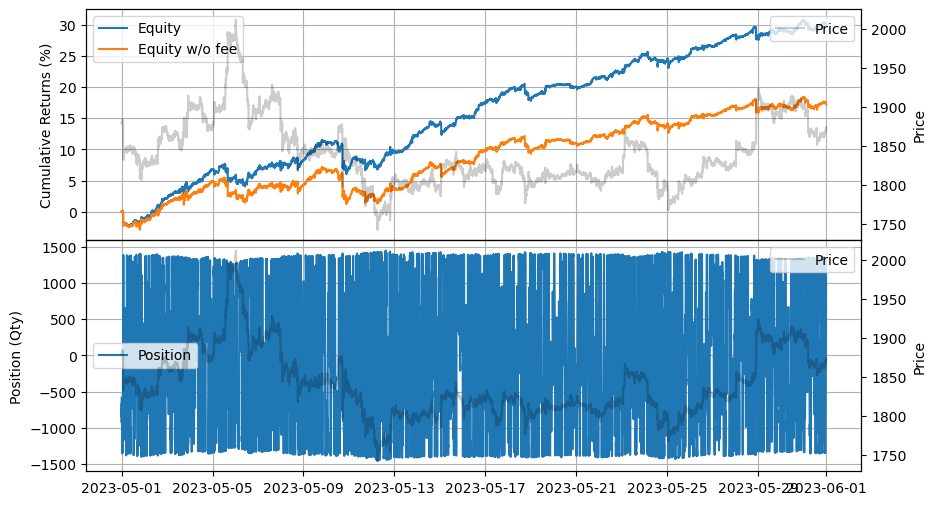

data = np.load('stats/obi_ethusdt.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

[6]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2023-05-01 00:00:00 | 2023-05-31 23:55:00 | 9.017874 | 11.140311 | 0.299582 | 0.055187 | 4112.621933 | 82.252375 | 5.428451 | 0.000118 | 2.6036e6 |

[7]:

stats.plot()

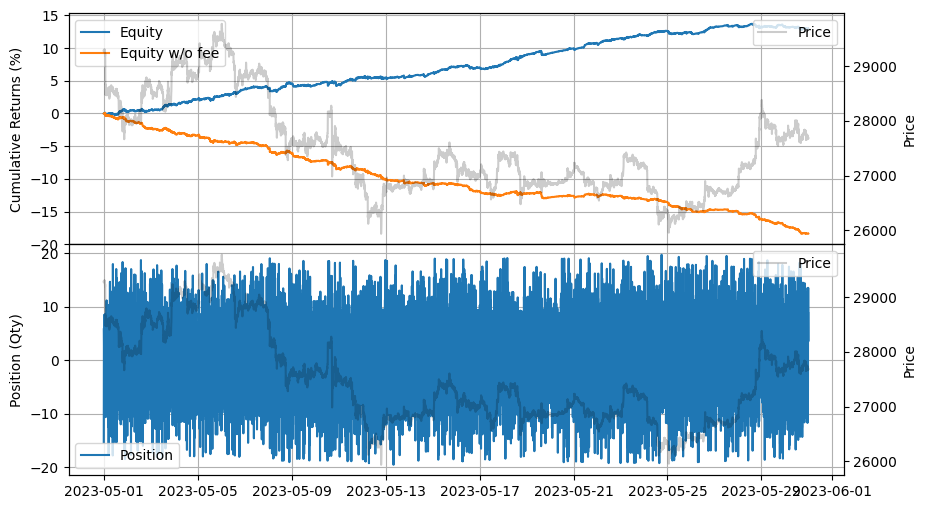

Another approach is to generate trading volume to qualify as a market maker and receive rebates. This strategy involves maintaining a high skew and tight spread. While the strategy itself may not be profitable or may incur losses, it can help achieve market maker status.

[9]:

%%time

roi_lb = 10000

roi_ub = 50000

latency_data = np.concatenate(

[np.load('latency/live_order_latency_{}.npz'.format(date))['data'] for date in range(20230501, 20230532)]

)

asset = (

BacktestAsset()

.data(['data2/btcusdt_{}.npz'.format(date) for date in range(20230501, 20230532)])

.initial_snapshot('data2/btcusdt_20230430_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(2)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 30_000_000)

half_spread = 10

skew = 2

c1 = 20

depth = 0.001 # 0.1% from the mid price

interval = 500_000_000 # 500ms

window = 600_000_000_000 / interval # 10min

order_qty_dollar = 25_000

max_position_dollar = order_qty_dollar * 20

grid_num = 1

grid_interval = hbt.depth(0).tick_size

obi_mm(

hbt,

recorder.recorder,

half_spread,

skew,

c1,

depth,

interval,

window,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

recorder.to_npz('stats/obi_vg_btcusdt.npz')

CPU times: user 30min 13s, sys: 44.1 s, total: 30min 57s

Wall time: 31min 2s

[10]:

data = np.load('stats/obi_vg_btcusdt.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=1_000_000)

)

stats.summary()

[10]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2023-05-01 00:00:00 | 2023-05-30 23:55:00 | 14.0088 | 17.366641 | 0.129901 | 0.00928 | 8368.135201 | 209.203461 | 13.998514 | 0.000021 | 536859.7998 |

[11]:

stats.plot()

Update on Backtesting Results for 2025

Updated backtesting results for February 2025 using the same parameters as in May 2023, except for the power_prob_queue_model parameter, which was changed from 2 to 3 to reflect market changes and a more challenging fill in the queue.

[13]:

import datetime

start_date = datetime.datetime.strptime('20250101', '%Y%m%d')

end_date = datetime.datetime.strptime('20250228', '%Y%m%d')

[14]:

%%time

roi_lb = 50000

roi_ub = 150000

latency_data = []

date = start_date

while date <= end_date:

latency_data.append('latency/order_latency_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

data = []

date = start_date

while date <= end_date:

data.append('data2/btcusdt_{}.npz'.format(date.strftime("%Y%m%d")))

date += datetime.timedelta(days=1)

asset = (

BacktestAsset()

.data(data)

.initial_snapshot('data2/btcusdt_20241231_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 30_000_000)

half_spread = 80

skew = 3.5

c1 = 160

depth = 0.025 # 2.5% from the mid price

interval = 1_000_000_000 # 1s

window = 3_600_000_000_000 / interval # 1hour

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 50

grid_num = 1

grid_interval = hbt.depth(0).tick_size

obi_mm(

hbt,

recorder.recorder,

half_spread,

skew,

c1,

depth,

interval,

window,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/obi_btcusdt_2025.npz')

CPU times: user 1h 56min 52s, sys: 8min 33s, total: 2h 5min 25s

Wall time: 1h 29min 36s

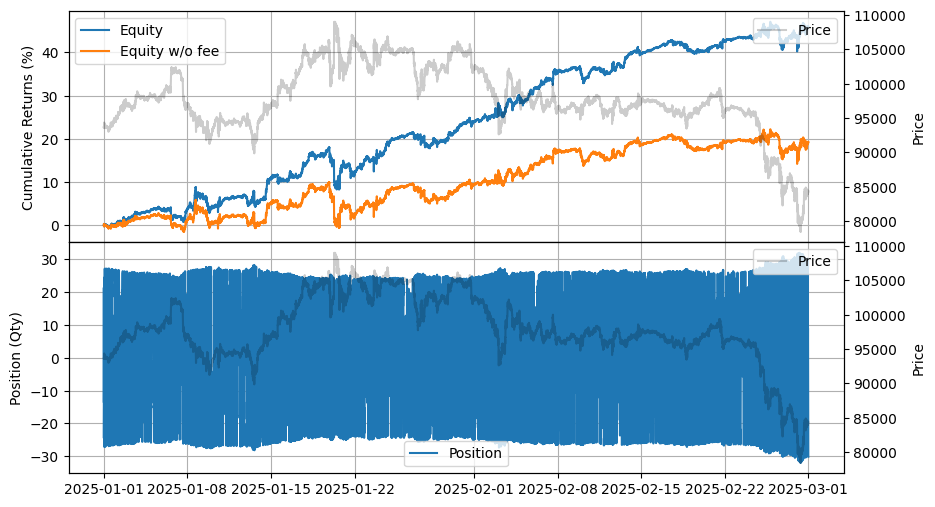

You can see from the following report that the order book imbalance continues to work consistently. However, the return per trade drops from 0.0139% to 0.0086%, including the 0.005% rebates. This again highlights the importance of rebates and the corresponding fee structure for market makers.

[16]:

data = np.load('stats/obi_btcusdt_2025.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

[16]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2025-01-01 00:00:00 | 2025-02-28 23:55:00 | 5.369875 | 7.198137 | 0.459649 | 0.097893 | 4533.741393 | 90.675217 | 4.695446 | 0.000086 | 2.6075e6 |

[17]:

stats.plot()

[2]:

data = np.load('stats/obi_btcusdt_202505.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

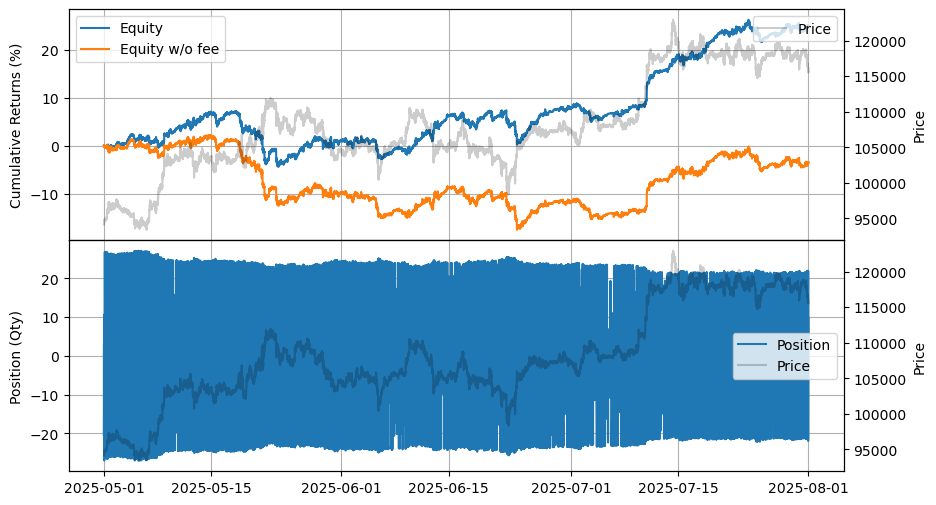

[2]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2025-05-01 00:00:00 | 2025-07-31 23:55:00 | 3.037498 | 4.129756 | 0.250298 | 0.115695 | 3095.899453 | 61.918439 | 2.16342 | 0.000044 | 2.5883e6 |

[3]:

stats.plot()

[3]: