Fusing Depth Data

Overview

Most cryptocurrency exchanges do not deliver true tick-by-tick Level-2 data. Instead, they provide conflated feeds in which individual order-book updates are aggregated over short intervals. For example, Binance Futures’ depth@0ms stream is still aggregated: You can confirm that its best-bid-offer (BBO) values update less frequently than those in the bookTicker stream, which captures every BBO change. Other venues state similar limitations explicitly—Bybit, for instance, publishes the

Level 1 data (BBO) every 10ms, the Level 50 data every 20ms, and the Level 200 data every 100ms.

To generate accurate fill simulations and realistic backtesting results, you must therefore fuse multiple depth streams into a single feed that preserves the highest possible update frequency and granularity.

Let’s see Binance Futures as our example.

Data Preparation

[1]:

# !wget https://datasets.tardis.dev/v1/binance-futures/trades/2025/05/01/BTCUSDT.csv.gz -O BTCUSDT_trades_20250501.csv.gz

# !wget https://datasets.tardis.dev/v1/binance-futures/incremental_book_L2/2025/05/01/BTCUSDT.csv.gz -O BTCUSDT_incremental_book_L2_20250501.csv.gz

# !wget https://datasets.tardis.dev/v1/binance-futures/book_ticker/2025/05/01/BTCUSDT.csv.gz -O BTCUSDT_book_ticker_20250501.csv.gz

[2]:

from hftbacktest.data.utils import tardis

tardis.convert(

[

'BTCUSDT_trades_20250501.csv.gz',

'BTCUSDT_incremental_book_L2_20250501.csv.gz'

],

output_filename='BTCUSDT_20250501.npz',

buffer_size=1_000_000_000,

snapshot_mode='process'

)

Reading BTCUSDT_trades_20250501.csv.gz

Reading BTCUSDT_incremental_book_L2_20250501.csv.gz

Correcting the latency

Correcting the event order

Saving to BTCUSDT_20250501.npz

[2]:

array([(3758096386, 1746057600043000000, 1746057600046245000, 94125.2, 1.0000e-02, 0, 0, 0.),

(3758096387, 1746057600072000000, 1746057601025373000, 93954.8, 0.0000e+00, 0, 0, 0.),

(3758096388, 1746057600072000000, 1746057601025373000, 94125.1, 1.0798e+01, 0, 0, 0.),

...,

(3758096385, 1746143999978000000, 1746143999980195000, 96406. , 1.5590e+00, 0, 0, 0.),

(3758096385, 1746143999978000000, 1746143999980195000, 96411.2, 6.1000e-02, 0, 0, 0.),

(3758096385, 1746143999978000000, 1746143999980195000, 96423.2, 1.0130e+01, 0, 0, 0.)],

shape=(106343798,), dtype={'names': ['ev', 'exch_ts', 'local_ts', 'px', 'qty', 'order_id', 'ival', 'fval'], 'formats': ['<u8', '<i8', '<i8', '<f8', '<f8', '<u8', '<i8', '<f8'], 'offsets': [0, 8, 16, 24, 32, 40, 48, 56], 'itemsize': 64, 'aligned': True})

Use the backtester to replay the data, get the BBO values from the Level-2 depth feed to compare it with the BBO obtained from the book ticker stream.

[3]:

import numpy as np

from numba import njit

from hftbacktest import (

BacktestAsset,

ROIVectorMarketDepthBacktest

)

@njit

def record_l2_bbo(

hbt,

timeout

):

asset_no = 0

t = 0

l2_bbo = np.full((30_000_000, 5), np.nan, np.float64)

prev_best_bid = np.nan

prev_best_ask = np.nan

prev_best_bid_qty = np.nan

prev_best_ask_qty = np.nan

# 0: Timeout(no market feed received within the timeout interval)

# 2: Market Feed

# Otherwise, an error occurs.

while hbt.wait_next_feed(False, timeout) in [0, 2]:

depth = hbt.depth(asset_no)

best_bid = depth.best_bid

best_ask = depth.best_ask

best_bid_qty = depth.bid_qty_at_tick(depth.best_bid_tick)

best_ask_qty = depth.ask_qty_at_tick(depth.best_ask_tick)

if (

best_bid != prev_best_bid

or best_ask != prev_best_ask

or best_bid_qty != prev_best_bid_qty

or best_ask_qty != prev_best_ask_qty

):

l2_bbo[t, 0] = hbt.current_timestamp

l2_bbo[t, 1] = prev_best_bid = best_bid

l2_bbo[t, 2] = prev_best_ask = best_ask

l2_bbo[t, 3] = prev_best_bid_qty = best_bid_qty

l2_bbo[t, 4] = prev_best_ask_qty = best_ask_qty

t += 1

if t >= len(l2_bbo):

raise Exception

return l2_bbo[:t]

[4]:

%%time

roi_lb = 50000

roi_ub = 150000

asset = (

BacktestAsset()

.data(['BTCUSDT_20250501.npz'])

.linear_asset(1.0)

.constant_order_latency(0, 0)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

timeout = 100_000_000 # 100ms

l2_bbo = record_l2_bbo(

hbt,

timeout

)

_ = hbt.close()

CPU times: user 40.5 s, sys: 4.34 s, total: 44.9 s

Wall time: 43.4 s

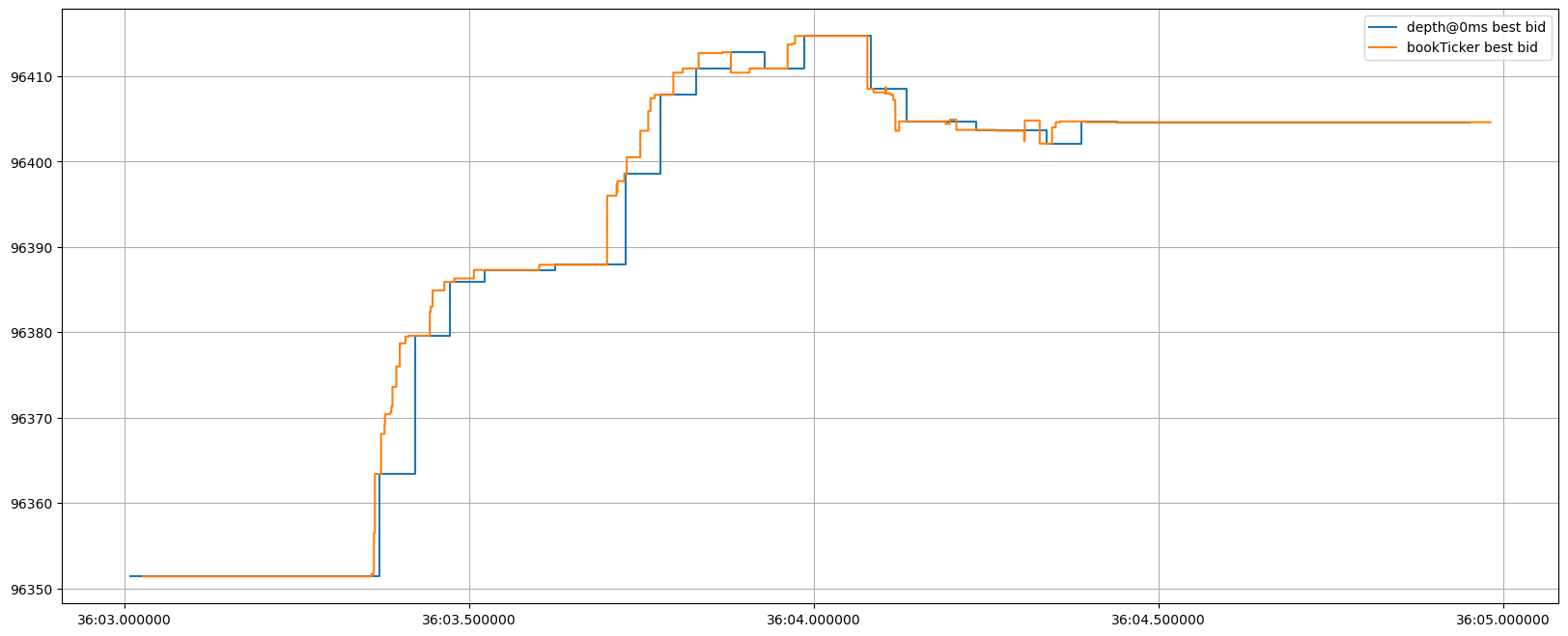

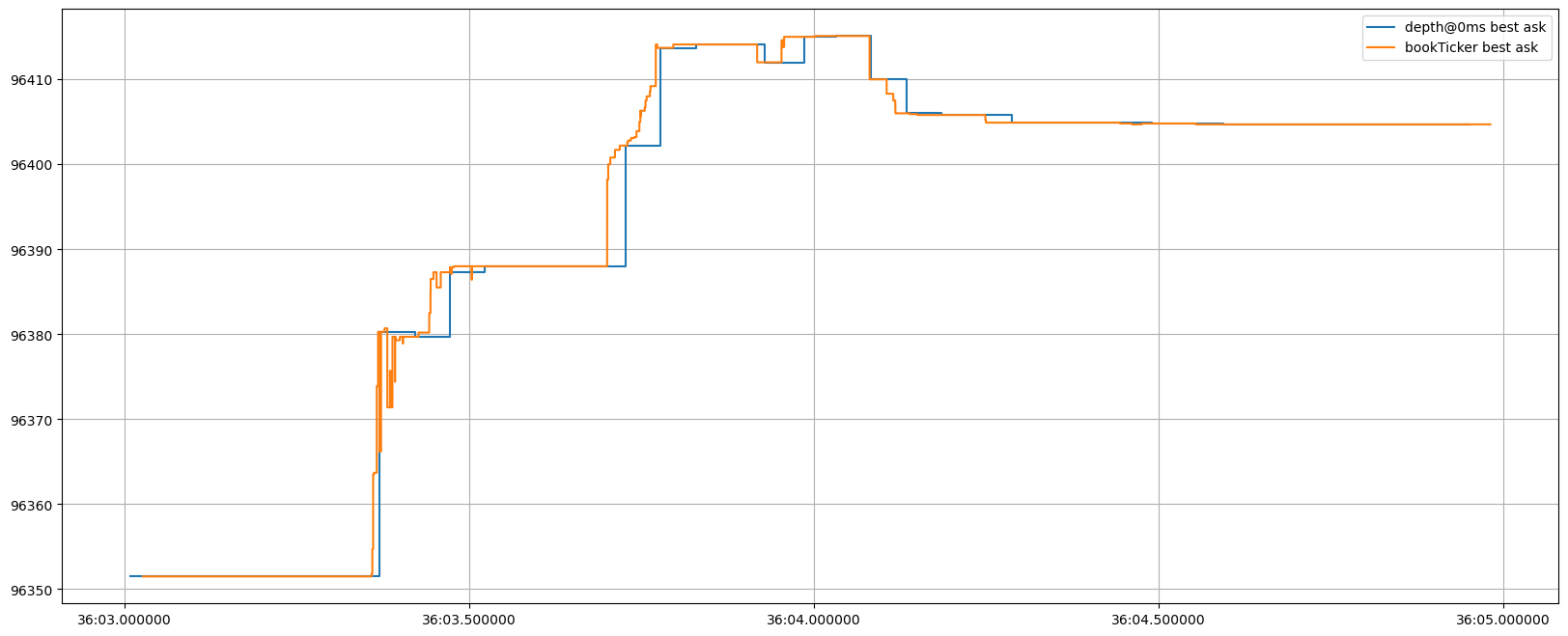

Comparing BBO updates: Level-2 (depth@0ms) Stream vs bookTicker Stream

The bookTicker stream delivers updates more often and leads the Level-2 feed by a small margin.

[5]:

import polars as pl

from matplotlib import pyplot as plt

[6]:

df_l2_bbo = pl.DataFrame(l2_bbo)

df_l2_bbo.columns = ['Local Timestamp', 'Bid', 'Ask', 'Bid Qty', 'Ask Qty']

df_l2_bbo = df_l2_bbo.with_columns(

pl.from_epoch('Local Timestamp', time_unit='ns')

).filter(

(pl.col('Local Timestamp') > pl.lit('2025-05-01 14:36:03').str.strptime(pl.Datetime, '%Y-%m-%d %H:%M:%S')) &

(pl.col('Local Timestamp') < pl.lit('2025-05-01 14:36:5').str.strptime(pl.Datetime, '%Y-%m-%d %H:%M:%S'))

)

[7]:

df_book_ticker = pl.read_csv('BTCUSDT_book_ticker_20250501.csv.gz').with_columns(

pl.from_epoch('local_timestamp', time_unit='us')

).select(

'local_timestamp', 'bid_price', 'ask_price', 'bid_amount', 'ask_amount'

).filter(

(pl.col('local_timestamp') > pl.lit('2025-05-01 14:36:03').str.strptime(pl.Datetime, '%Y-%m-%d %H:%M:%S')) &

(pl.col('local_timestamp') < pl.lit('2025-05-01 14:36:5').str.strptime(pl.Datetime, '%Y-%m-%d %H:%M:%S'))

)

[8]:

plt.figure(figsize=(20, 8))

plt.step(df_l2_bbo['Local Timestamp'], df_l2_bbo['Bid'], where='post')

plt.step(df_book_ticker['local_timestamp'], df_book_ticker['bid_price'], where='post')

plt.legend(['depth@0ms best bid', 'bookTicker best bid'])

plt.grid()

[9]:

plt.figure(figsize=(20, 8))

plt.step(df_l2_bbo['Local Timestamp'], df_l2_bbo['Ask'], where='post')

plt.step(df_book_ticker['local_timestamp'], df_book_ticker['ask_price'], where='post')

plt.legend(['depth@0ms best ask', 'bookTicker best ask'])

plt.grid()

You’ll notice that the bookTicker stream delivers updates far more frequently—especially when you factor in changes to both price and quantity.

[10]:

with pl.Config(tbl_rows=100):

print(df_l2_bbo)

shape: (39, 5)

┌───────────────────────────────┬─────────┬─────────┬─────────┬─────────┐

│ Local Timestamp ┆ Bid ┆ Ask ┆ Bid Qty ┆ Ask Qty │

│ --- ┆ --- ┆ --- ┆ --- ┆ --- │

│ datetime[ns] ┆ f64 ┆ f64 ┆ f64 ┆ f64 │

╞═══════════════════════════════╪═════════╪═════════╪═════════╪═════════╡

│ 2025-05-01 14:36:03.008176128 ┆ 96351.4 ┆ 96351.5 ┆ 6.344 ┆ 7.159 │

│ 2025-05-01 14:36:03.060811008 ┆ 96351.4 ┆ 96351.5 ┆ 6.368 ┆ 1.297 │

│ 2025-05-01 14:36:03.112276992 ┆ 96351.4 ┆ 96351.5 ┆ 6.528 ┆ 0.128 │

│ 2025-05-01 14:36:03.163234048 ┆ 96351.4 ┆ 96351.5 ┆ 6.878 ┆ 0.188 │

│ 2025-05-01 14:36:03.215074048 ┆ 96351.4 ┆ 96351.5 ┆ 6.584 ┆ 2.819 │

│ 2025-05-01 14:36:03.266274048 ┆ 96351.4 ┆ 96351.5 ┆ 6.399 ┆ 1.996 │

│ 2025-05-01 14:36:03.316154112 ┆ 96351.4 ┆ 96351.5 ┆ 6.399 ┆ 2.127 │

│ 2025-05-01 14:36:03.369733888 ┆ 96363.4 ┆ 96380.3 ┆ 1.12 ┆ 0.006 │

│ 2025-05-01 14:36:03.421906944 ┆ 96379.6 ┆ 96379.7 ┆ 0.438 ┆ 0.036 │

│ 2025-05-01 14:36:03.472250880 ┆ 96385.9 ┆ 96387.3 ┆ 0.876 ┆ 0.201 │

│ 2025-05-01 14:36:03.522233088 ┆ 96387.3 ┆ 96388.0 ┆ 0.029 ┆ 0.034 │

│ 2025-05-01 14:36:03.573129984 ┆ 96387.3 ┆ 96388.0 ┆ 0.446 ┆ 0.235 │

│ 2025-05-01 14:36:03.624218112 ┆ 96387.9 ┆ 96388.0 ┆ 1.641 ┆ 1.045 │

│ 2025-05-01 14:36:03.675269120 ┆ 96387.9 ┆ 96388.0 ┆ 8.122 ┆ 1.654 │

│ 2025-05-01 14:36:03.726845952 ┆ 96398.6 ┆ 96402.2 ┆ 0.311 ┆ 0.116 │

│ 2025-05-01 14:36:03.777195008 ┆ 96407.8 ┆ 96413.7 ┆ 0.46 ┆ 0.104 │

│ 2025-05-01 14:36:03.829007104 ┆ 96410.9 ┆ 96414.1 ┆ 0.36 ┆ 0.981 │

│ 2025-05-01 14:36:03.879574016 ┆ 96412.8 ┆ 96414.1 ┆ 0.291 ┆ 0.016 │

│ 2025-05-01 14:36:03.929277952 ┆ 96410.9 ┆ 96412.0 ┆ 0.852 ┆ 0.005 │

│ 2025-05-01 14:36:03.985562880 ┆ 96414.7 ┆ 96415.0 ┆ 0.07 ┆ 0.005 │

│ 2025-05-01 14:36:04.032508928 ┆ 96414.7 ┆ 96415.1 ┆ 5.581 ┆ 0.06 │

│ 2025-05-01 14:36:04.082749952 ┆ 96408.5 ┆ 96410.0 ┆ 0.388 ┆ 0.025 │

│ 2025-05-01 14:36:04.134117120 ┆ 96404.7 ┆ 96406.0 ┆ 0.002 ┆ 0.65 │

│ 2025-05-01 14:36:04.185359104 ┆ 96404.7 ┆ 96405.8 ┆ 0.002 ┆ 0.37 │

│ 2025-05-01 14:36:04.235608064 ┆ 96403.7 ┆ 96405.8 ┆ 0.02 ┆ 0.783 │

│ 2025-05-01 14:36:04.287187968 ┆ 96403.6 ┆ 96404.9 ┆ 0.249 ┆ 2.194 │

│ 2025-05-01 14:36:04.338068992 ┆ 96402.1 ┆ 96404.9 ┆ 0.042 ┆ 3.069 │

│ 2025-05-01 14:36:04.388464128 ┆ 96404.7 ┆ 96404.9 ┆ 0.13 ┆ 2.421 │

│ 2025-05-01 14:36:04.440344064 ┆ 96404.6 ┆ 96404.9 ┆ 0.435 ┆ 4.269 │

│ 2025-05-01 14:36:04.490669056 ┆ 96404.6 ┆ 96404.8 ┆ 0.603 ┆ 1.21 │

│ 2025-05-01 14:36:04.541093120 ┆ 96404.6 ┆ 96404.8 ┆ 0.839 ┆ 3.744 │

│ 2025-05-01 14:36:04.594004992 ┆ 96404.6 ┆ 96404.7 ┆ 0.841 ┆ 0.761 │

│ 2025-05-01 14:36:04.644099072 ┆ 96404.6 ┆ 96404.7 ┆ 0.961 ┆ 2.639 │

│ 2025-05-01 14:36:04.694644992 ┆ 96404.6 ┆ 96404.7 ┆ 5.782 ┆ 3.732 │

│ 2025-05-01 14:36:04.746102016 ┆ 96404.6 ┆ 96404.7 ┆ 6.503 ┆ 6.072 │

│ 2025-05-01 14:36:04.797575936 ┆ 96404.6 ┆ 96404.7 ┆ 6.541 ┆ 6.28 │

│ 2025-05-01 14:36:04.848253952 ┆ 96404.6 ┆ 96404.7 ┆ 5.084 ┆ 7.323 │

│ 2025-05-01 14:36:04.898958080 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.868 │

│ 2025-05-01 14:36:04.951334912 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.284 │

└───────────────────────────────┴─────────┴─────────┴─────────┴─────────┘

[11]:

with pl.Config(tbl_rows=100):

print(df_book_ticker)

shape: (1_432, 5)

┌────────────────────────────┬───────────┬───────────┬────────────┬────────────┐

│ local_timestamp ┆ bid_price ┆ ask_price ┆ bid_amount ┆ ask_amount │

│ --- ┆ --- ┆ --- ┆ --- ┆ --- │

│ datetime[μs] ┆ f64 ┆ f64 ┆ f64 ┆ f64 │

╞════════════════════════════╪═══════════╪═══════════╪════════════╪════════════╡

│ 2025-05-01 14:36:03.027063 ┆ 96351.4 ┆ 96351.5 ┆ 6.338 ┆ 7.157 │

│ 2025-05-01 14:36:03.027070 ┆ 96351.4 ┆ 96351.5 ┆ 6.338 ┆ 7.154 │

│ 2025-05-01 14:36:03.027072 ┆ 96351.4 ┆ 96351.5 ┆ 6.338 ┆ 7.121 │

│ 2025-05-01 14:36:03.029315 ┆ 96351.4 ┆ 96351.5 ┆ 6.35 ┆ 7.121 │

│ 2025-05-01 14:36:03.030317 ┆ 96351.4 ┆ 96351.5 ┆ 6.338 ┆ 7.121 │

│ 2025-05-01 14:36:03.045954 ┆ 96351.4 ┆ 96351.5 ┆ 6.338 ┆ 7.119 │

│ 2025-05-01 14:36:03.049547 ┆ 96351.4 ┆ 96351.5 ┆ 6.348 ┆ 7.119 │

│ 2025-05-01 14:36:03.050625 ┆ 96351.4 ┆ 96351.5 ┆ 6.348 ┆ 4.174 │

│ 2025-05-01 14:36:03.050627 ┆ 96351.4 ┆ 96351.5 ┆ 6.348 ┆ 2.452 │

│ 2025-05-01 14:36:03.050627 ┆ 96351.4 ┆ 96351.5 ┆ 6.348 ┆ 2.395 │

│ 2025-05-01 14:36:03.051616 ┆ 96351.4 ┆ 96351.5 ┆ 6.348 ┆ 1.764 │

│ 2025-05-01 14:36:03.052630 ┆ 96351.4 ┆ 96351.5 ┆ 6.358 ┆ 1.764 │

│ 2025-05-01 14:36:03.052633 ┆ 96351.4 ┆ 96351.5 ┆ 6.358 ┆ 1.762 │

│ 2025-05-01 14:36:03.052634 ┆ 96351.4 ┆ 96351.5 ┆ 6.358 ┆ 1.764 │

│ 2025-05-01 14:36:03.053796 ┆ 96351.4 ┆ 96351.5 ┆ 6.36 ┆ 1.764 │

│ 2025-05-01 14:36:03.053797 ┆ 96351.4 ┆ 96351.5 ┆ 6.36 ┆ 1.762 │

│ 2025-05-01 14:36:03.054626 ┆ 96351.4 ┆ 96351.5 ┆ 6.354 ┆ 1.762 │

│ 2025-05-01 14:36:03.054629 ┆ 96351.4 ┆ 96351.5 ┆ 6.354 ┆ 1.737 │

│ 2025-05-01 14:36:03.054634 ┆ 96351.4 ┆ 96351.5 ┆ 6.354 ┆ 1.349 │

│ 2025-05-01 14:36:03.055714 ┆ 96351.4 ┆ 96351.5 ┆ 6.364 ┆ 1.349 │

│ 2025-05-01 14:36:03.056808 ┆ 96351.4 ┆ 96351.5 ┆ 6.364 ┆ 1.297 │

│ 2025-05-01 14:36:03.059917 ┆ 96351.4 ┆ 96351.5 ┆ 6.366 ┆ 1.297 │

│ 2025-05-01 14:36:03.059917 ┆ 96351.4 ┆ 96351.5 ┆ 6.368 ┆ 1.297 │

│ 2025-05-01 14:36:03.064652 ┆ 96351.4 ┆ 96351.5 ┆ 6.368 ┆ 1.201 │

│ 2025-05-01 14:36:03.064653 ┆ 96351.4 ┆ 96351.5 ┆ 6.368 ┆ 1.087 │

│ 2025-05-01 14:36:03.064656 ┆ 96351.4 ┆ 96351.5 ┆ 6.368 ┆ 1.038 │

│ 2025-05-01 14:36:03.064660 ┆ 96351.4 ┆ 96351.5 ┆ 6.368 ┆ 0.937 │

│ 2025-05-01 14:36:03.064661 ┆ 96351.4 ┆ 96351.5 ┆ 6.368 ┆ 0.679 │

│ 2025-05-01 14:36:03.064663 ┆ 96351.4 ┆ 96351.5 ┆ 6.368 ┆ 0.592 │

│ 2025-05-01 14:36:03.067917 ┆ 96351.4 ┆ 96351.5 ┆ 6.368 ┆ 0.702 │

│ 2025-05-01 14:36:03.069890 ┆ 96351.4 ┆ 96351.5 ┆ 6.498 ┆ 0.702 │

│ 2025-05-01 14:36:03.071890 ┆ 96351.4 ┆ 96351.5 ┆ 6.492 ┆ 0.702 │

│ 2025-05-01 14:36:03.071894 ┆ 96351.4 ┆ 96351.5 ┆ 6.492 ┆ 0.592 │

│ 2025-05-01 14:36:03.071897 ┆ 96351.4 ┆ 96351.5 ┆ 6.498 ┆ 0.592 │

│ 2025-05-01 14:36:03.074200 ┆ 96351.4 ┆ 96351.5 ┆ 6.498 ┆ 0.702 │

│ 2025-05-01 14:36:03.078112 ┆ 96351.4 ┆ 96351.5 ┆ 6.508 ┆ 0.702 │

│ 2025-05-01 14:36:03.092415 ┆ 96351.4 ┆ 96351.5 ┆ 6.508 ┆ 0.592 │

│ 2025-05-01 14:36:03.095210 ┆ 96351.4 ┆ 96351.5 ┆ 6.858 ┆ 0.592 │

│ 2025-05-01 14:36:03.097268 ┆ 96351.4 ┆ 96351.5 ┆ 6.868 ┆ 0.592 │

│ 2025-05-01 14:36:03.097274 ┆ 96351.4 ┆ 96351.5 ┆ 6.862 ┆ 0.592 │

│ 2025-05-01 14:36:03.097277 ┆ 96351.4 ┆ 96351.5 ┆ 6.868 ┆ 0.592 │

│ 2025-05-01 14:36:03.098526 ┆ 96351.4 ┆ 96351.5 ┆ 6.878 ┆ 0.592 │

│ 2025-05-01 14:36:03.099564 ┆ 96351.4 ┆ 96351.5 ┆ 6.878 ┆ 0.385 │

│ 2025-05-01 14:36:03.099566 ┆ 96351.4 ┆ 96351.5 ┆ 6.878 ┆ 0.178 │

│ 2025-05-01 14:36:03.102809 ┆ 96351.4 ┆ 96351.5 ┆ 6.878 ┆ 0.147 │

│ 2025-05-01 14:36:03.102809 ┆ 96351.4 ┆ 96351.5 ┆ 6.878 ┆ 0.145 │

│ 2025-05-01 14:36:03.102840 ┆ 96351.4 ┆ 96351.5 ┆ 6.878 ┆ 0.124 │

│ 2025-05-01 14:36:03.104977 ┆ 96351.4 ┆ 96351.5 ┆ 6.878 ┆ 0.126 │

│ 2025-05-01 14:36:03.105552 ┆ 96351.4 ┆ 96351.5 ┆ 6.878 ┆ 0.128 │

│ 2025-05-01 14:36:03.108741 ┆ 96351.4 ┆ 96351.5 ┆ 6.528 ┆ 0.128 │

│ … ┆ … ┆ … ┆ … ┆ … │

│ 2025-05-01 14:36:04.888094 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 5.431 │

│ 2025-05-01 14:36:04.888317 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 5.051 │

│ 2025-05-01 14:36:04.888318 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.335 │

│ 2025-05-01 14:36:04.888320 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.323 │

│ 2025-05-01 14:36:04.888773 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 3.517 │

│ 2025-05-01 14:36:04.888778 ┆ 96404.6 ┆ 96404.7 ┆ 5.117 ┆ 3.517 │

│ 2025-05-01 14:36:04.888779 ┆ 96404.6 ┆ 96404.7 ┆ 5.117 ┆ 3.567 │

│ 2025-05-01 14:36:04.890093 ┆ 96404.6 ┆ 96404.7 ┆ 5.117 ┆ 3.217 │

│ 2025-05-01 14:36:04.890110 ┆ 96404.6 ┆ 96404.7 ┆ 5.117 ┆ 3.248 │

│ 2025-05-01 14:36:04.890111 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 3.248 │

│ 2025-05-01 14:36:04.890749 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 3.25 │

│ 2025-05-01 14:36:04.890756 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 3.253 │

│ 2025-05-01 14:36:04.890757 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 3.703 │

│ 2025-05-01 14:36:04.890758 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 3.701 │

│ 2025-05-01 14:36:04.893901 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 3.703 │

│ 2025-05-01 14:36:04.894774 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.208 │

│ 2025-05-01 14:36:04.894778 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.207 │

│ 2025-05-01 14:36:04.896090 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.208 │

│ 2025-05-01 14:36:04.898233 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.868 │

│ 2025-05-01 14:36:04.900924 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 5.218 │

│ 2025-05-01 14:36:04.900929 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.868 │

│ 2025-05-01 14:36:04.900930 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.867 │

│ 2025-05-01 14:36:04.902011 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.868 │

│ 2025-05-01 14:36:04.917421 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.934 │

│ 2025-05-01 14:36:04.919464 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.933 │

│ 2025-05-01 14:36:04.919471 ┆ 96404.6 ┆ 96404.7 ┆ 5.107 ┆ 4.934 │

│ 2025-05-01 14:36:04.931723 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 4.934 │

│ 2025-05-01 14:36:04.946773 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.284 │

│ 2025-05-01 14:36:04.946775 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.286 │

│ 2025-05-01 14:36:04.946779 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.809 │

│ 2025-05-01 14:36:04.948089 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.459 │

│ 2025-05-01 14:36:04.948091 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 4.936 │

│ 2025-05-01 14:36:04.948114 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 4.935 │

│ 2025-05-01 14:36:04.949397 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 4.933 │

│ 2025-05-01 14:36:04.949402 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 4.934 │

│ 2025-05-01 14:36:04.949405 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 4.932 │

│ 2025-05-01 14:36:04.949408 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.282 │

│ 2025-05-01 14:36:04.950159 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.284 │

│ 2025-05-01 14:36:04.951337 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 4.934 │

│ 2025-05-01 14:36:04.952587 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 4.932 │

│ 2025-05-01 14:36:04.954760 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.302 │

│ 2025-05-01 14:36:04.955915 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.301 │

│ 2025-05-01 14:36:04.956673 ┆ 96404.6 ┆ 96404.7 ┆ 5.001 ┆ 5.302 │

│ 2025-05-01 14:36:04.960766 ┆ 96404.6 ┆ 96404.7 ┆ 5.003 ┆ 5.302 │

│ 2025-05-01 14:36:04.970154 ┆ 96404.6 ┆ 96404.7 ┆ 5.003 ┆ 5.3 │

│ 2025-05-01 14:36:04.978932 ┆ 96404.6 ┆ 96404.7 ┆ 5.109 ┆ 5.3 │

│ 2025-05-01 14:36:04.981128 ┆ 96404.6 ┆ 96404.7 ┆ 5.109 ┆ 5.297 │

│ 2025-05-01 14:36:04.981130 ┆ 96404.6 ┆ 96404.7 ┆ 5.103 ┆ 5.297 │

│ 2025-05-01 14:36:04.981131 ┆ 96404.6 ┆ 96404.7 ┆ 5.103 ┆ 5.295 │

│ 2025-05-01 14:36:04.981142 ┆ 96404.6 ┆ 96404.7 ┆ 5.109 ┆ 5.295 │

└────────────────────────────┴───────────┴───────────┴────────────┴────────────┘

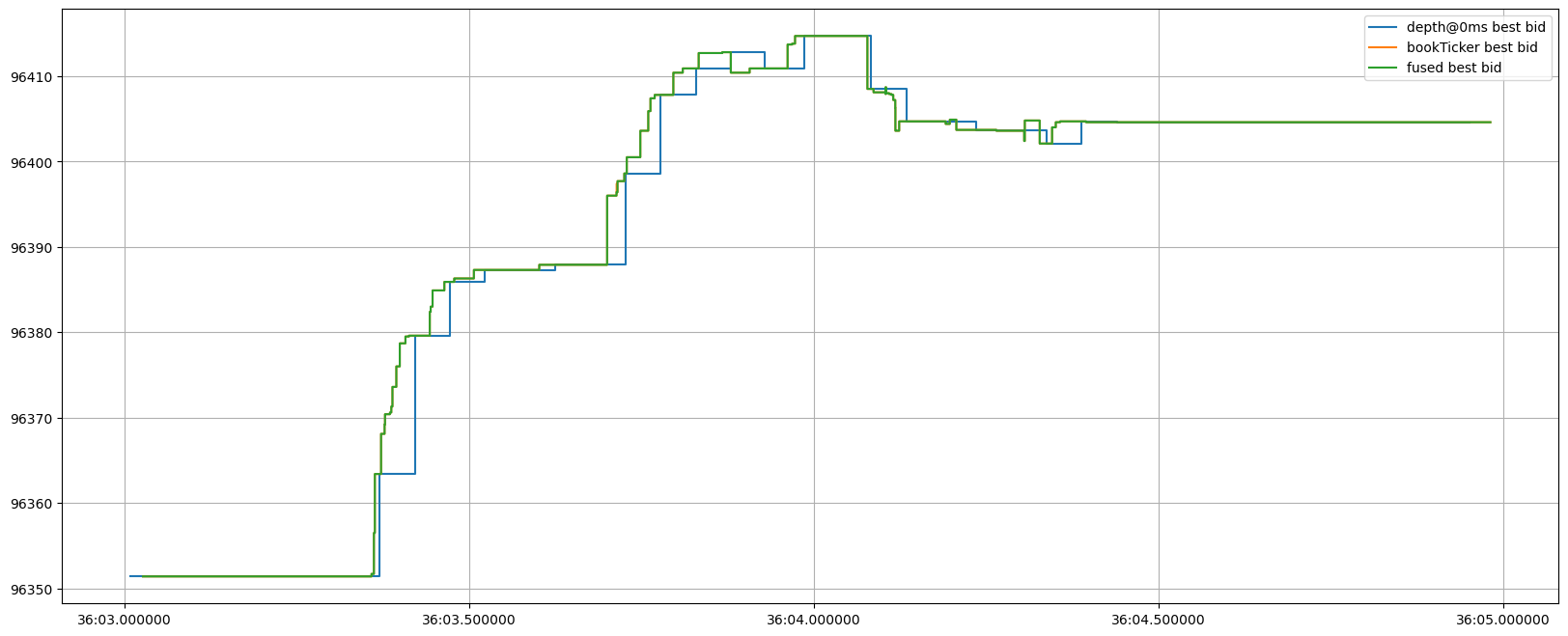

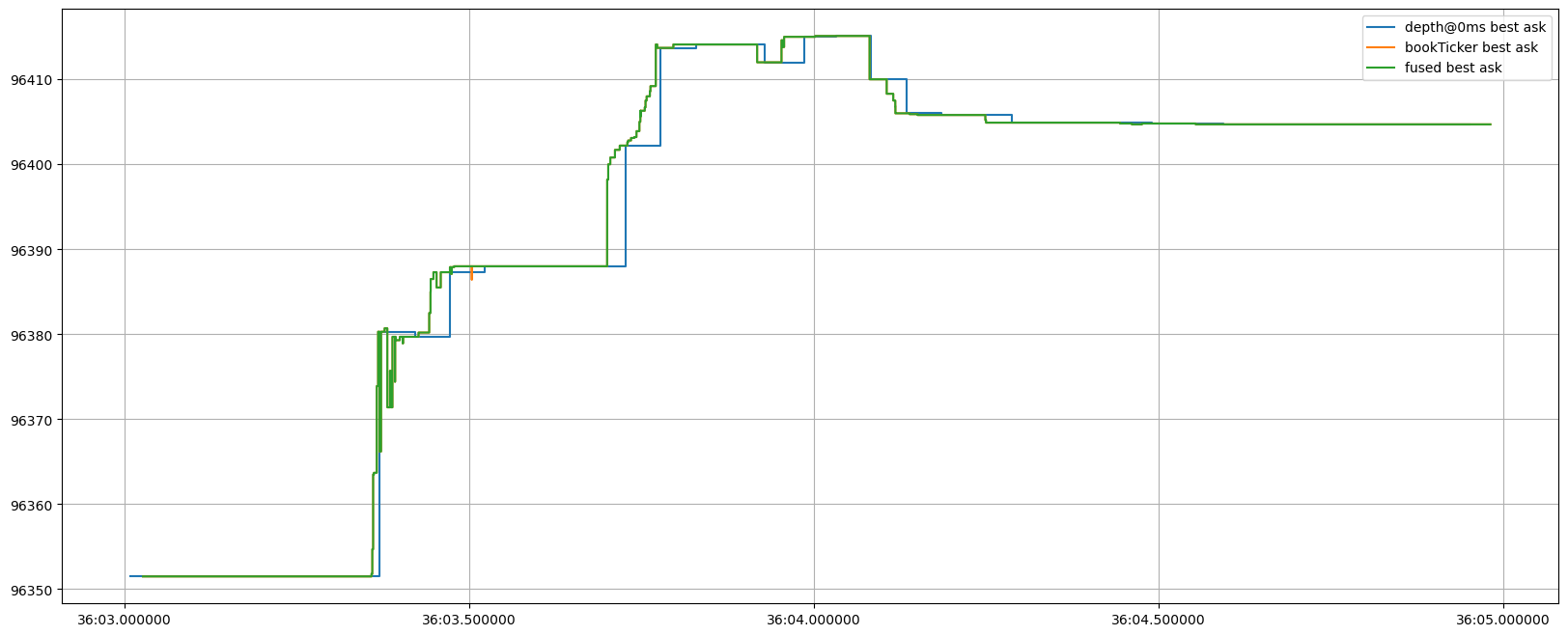

Fusing Multiple Depth Feeds

To obtain the most frequent and fine-grained market depth updates, it is necessary to combine the depth feed with the book ticker feed. The `FuseMarketDepth <https://hftbacktest.readthedocs.io/en/latest/reference/data_utilities.html#hftbacktest.binding.FuseMarketDepth>`__ utility helps fuse multiple depth update streams into a single order book view. HftBacktest includes a fused converter function

`convert_fuse <https://hftbacktest.readthedocs.io/en/latest/reference/hftbacktest.data.utils.tardis.html#hftbacktest.data.utils.tardis.convert_fuse>`__ for Tardis data.

However, this utility builds only a single consolidated order book, where:

Updates are processed in order of local receipt time.

The price-level information are updated based on the exchange timestamp.

If an older exchange-timestamped update arrives after a newer one for the same price level, it is discarded. This approach may lead to slight discrepancies between the local order book state and the actual state on the exchange.

For example:

A depth feed may show a best bid/ask (BBO) at 10/11.

A more current book ticker feed may show BBO at 10/14.

When fused:

The resulting book shows BBO at 10/14. But price levels above 14 (e.g., 15 and higher) still reflect outdated data from the original depth feed. This results in a partially updated and inconsistent order book. To maintain consistency with the depth feed’s original intent, you would need to build and maintain a separate order book for each feed.

[12]:

from hftbacktest.data.utils.tardis import convert_fuse

convert_fuse(

'BTCUSDT_trades_20250501.csv.gz',

'BTCUSDT_incremental_book_L2_20250501.csv.gz',

'BTCUSDT_book_ticker_20250501.csv.gz',

tick_size=0.1,

lot_size=0.001,

output_filename='BTCUSDT_fused_20250501.npz'

)

Correcting the latency

Correcting the event order

Saving to BTCUSDT_fused_20250501.npz

[12]:

array([(3489660929, 1746057600036000000, 1746057600038318000, 94125.2, 9.7830e+00, 0, 0, 0.),

(3758096385, 1746057600036000000, 1746057600038318000, 94125.1, 1.0882e+01, 0, 0, 0.),

(2684354562, 1746057600043000000, 1746057600046245000, 94125.2, 1.0000e-02, 0, 0, 0.),

...,

(3758096385, 1746143999978000000, 1746143999980195000, 96423.2, 1.0130e+01, 0, 0, 0.),

(3758096385, 1746143999979000000, 1746143999982227000, 96423.2, 9.8140e+00, 0, 0, 0.),

(3758096385, 1746143999982000000, 1746143999985629000, 96423.2, 9.8170e+00, 0, 0, 0.)],

shape=(123281421,), dtype={'names': ['ev', 'exch_ts', 'local_ts', 'px', 'qty', 'order_id', 'ival', 'fval'], 'formats': ['<u8', '<i8', '<i8', '<f8', '<f8', '<u8', '<i8', '<f8'], 'offsets': [0, 8, 16, 24, 32, 40, 48, 56], 'itemsize': 64, 'aligned': True})

[13]:

roi_lb = 50000

roi_ub = 150000

asset = (

BacktestAsset()

.data(['BTCUSDT_fused_20250501.npz'])

.linear_asset(1.0)

.constant_order_latency(0, 0)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

timeout = 100_000_000 # 100ms

l2_bbo_fused = record_l2_bbo(

hbt,

timeout

)

_ = hbt.close()

[14]:

df_l2_bbo_fused = pl.DataFrame(l2_bbo_fused)

df_l2_bbo_fused.columns = ['Local Timestamp', 'Bid', 'Ask', 'Bid Qty', 'Ask Qty']

df_l2_bbo_fused = df_l2_bbo_fused.with_columns(

pl.from_epoch('Local Timestamp', time_unit='ns')

).filter(

(pl.col('Local Timestamp') > pl.lit('2025-05-01 14:36:03').str.strptime(pl.Datetime, '%Y-%m-%d %H:%M:%S')) &

(pl.col('Local Timestamp') < pl.lit('2025-05-01 14:36:5').str.strptime(pl.Datetime, '%Y-%m-%d %H:%M:%S'))

)

[15]:

plt.figure(figsize=(20, 8))

plt.step(df_l2_bbo['Local Timestamp'], df_l2_bbo['Bid'], where='post')

plt.step(df_book_ticker['local_timestamp'], df_book_ticker['bid_price'], where='post')

plt.step(df_l2_bbo_fused['Local Timestamp'], df_l2_bbo_fused['Bid'], where='post')

plt.legend(['depth@0ms best bid', 'bookTicker best bid', 'fused best bid'])

plt.grid()

[16]:

plt.figure(figsize=(20, 8))

plt.step(df_l2_bbo['Local Timestamp'], df_l2_bbo['Ask'], where='post')

plt.step(df_book_ticker['local_timestamp'], df_book_ticker['ask_price'], where='post')

plt.step(df_l2_bbo_fused['Local Timestamp'], df_l2_bbo_fused['Ask'], where='post')

plt.legend(['depth@0ms best ask', 'bookTicker best ask', 'fused best ask'])

plt.grid()

Backtest Results Comparison

We now compare backtesting results between fused and non-fused data.

[17]:

from numba import uint64

from numba.typed import Dict

from hftbacktest import (

GTX,

LIMIT,

BUY,

SELL,

Recorder

)

from hftbacktest.stats import LinearAssetRecord

@njit

def basic_mm(

hbt,

stat,

half_spread,

skew,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval

):

asset_no = 0

tick_size = hbt.depth(0).tick_size

lot_size = hbt.depth(0).lot_size

while hbt.elapse(interval) == 0:

hbt.clear_inactive_orders(asset_no)

orders = hbt.orders(asset_no)

depth = hbt.depth(asset_no)

position = hbt.position(asset_no)

best_bid = depth.best_bid

best_ask = depth.best_ask

mid_price = (best_bid + best_ask) / 2.0

mid_price_tick = (depth.best_bid_tick + depth.best_ask_tick) / 2.0

#--------------------------------------------------------

# Computes bid price and ask price.

order_qty = max(round((order_qty_dollar / mid_price) / lot_size) * lot_size, lot_size)

normalized_position = position / order_qty

relative_bid_depth = half_spread + skew * normalized_position

relative_ask_depth = half_spread - skew * normalized_position

bid_price = min(mid_price * (1.0 - relative_bid_depth), best_bid)

ask_price = max(mid_price * (1.0 + relative_ask_depth), best_ask)

bid_price = np.floor(bid_price / tick_size) * tick_size

ask_price = np.ceil(ask_price / tick_size) * tick_size

#--------------------------------------------------------

# Updates quotes.

# Creates a new grid for buy orders.

new_bid_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price < max_position_dollar and np.isfinite(bid_price):

for i in range(grid_num):

bid_price_tick = round(bid_price / tick_size)

# order price in tick is used as order id.

new_bid_orders[uint64(bid_price_tick)] = bid_price

bid_price -= grid_interval

# Creates a new grid for sell orders.

new_ask_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price > -max_position_dollar and np.isfinite(ask_price):

for i in range(grid_num):

ask_price_tick = round(ask_price / tick_size)

# order price in tick is used as order id.

new_ask_orders[uint64(ask_price_tick)] = ask_price

ask_price += grid_interval

order_values = orders.values();

while order_values.has_next():

order = order_values.get()

# Cancels if a working order is not in the new grid.

if order.cancellable:

if (

(order.side == BUY and order.order_id not in new_bid_orders)

or (order.side == SELL and order.order_id not in new_ask_orders)

):

hbt.cancel(asset_no, order.order_id, False)

for order_id, order_price in new_bid_orders.items():

# Posts a new buy order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_buy_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

for order_id, order_price in new_ask_orders.items():

# Posts a new sell order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_sell_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

# Records the current state for stat calculation.

stat.record(hbt)

[18]:

roi_lb = 50000

roi_ub = 150000

half_spread = 0.0005 # a ratio relative to the fair price

skew = half_spread / 20

interval = 100_000_000 # in nanoseconds. 100ms

order_qty_dollar = 50_000

max_position_dollar = 1_000_000

grid_num = 1

grid_interval = 0.1

asset = (

BacktestAsset()

.data(['BTCUSDT_nonfused_20250501.npz'])

.linear_asset(1.0)

.intp_order_latency(['../latency/order_latency_20250501.npz'])

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

basic_mm(

hbt,

recorder.recorder,

half_spread,

skew,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval

)

_ = hbt.close()

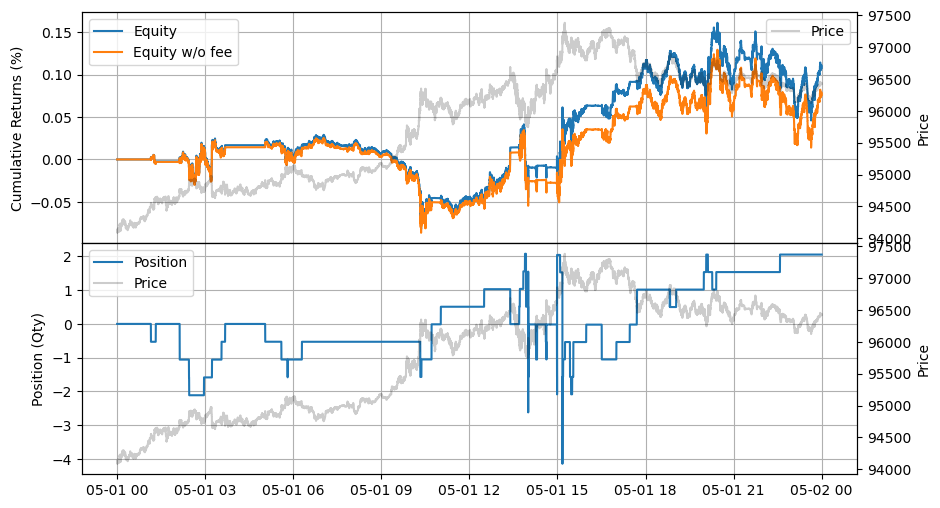

Backtesting with Non-Fused Data

[19]:

data = recorder.get(0)

stats = (

LinearAssetRecord(data)

.resample('1s')

.stats(book_size=1_000_000)

)

stats.summary()

[19]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2025-05-01 00:00:00 | 2025-05-01 23:59:59 | 11.17529 | 15.92313 | 0.001077 | 0.00115 | 128.001481 | 6.4003 | 0.936022 | 0.000168 | 402046.58425 |

[20]:

stats.plot()

[20]:

[21]:

asset = (

BacktestAsset()

.data(['BTCUSDT_fused_20250501.npz'])

.linear_asset(1.0)

.intp_order_latency(['../latency/order_latency_20250501.npz'])

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

basic_mm(

hbt,

recorder.recorder,

half_spread,

skew,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval

)

_ = hbt.close()

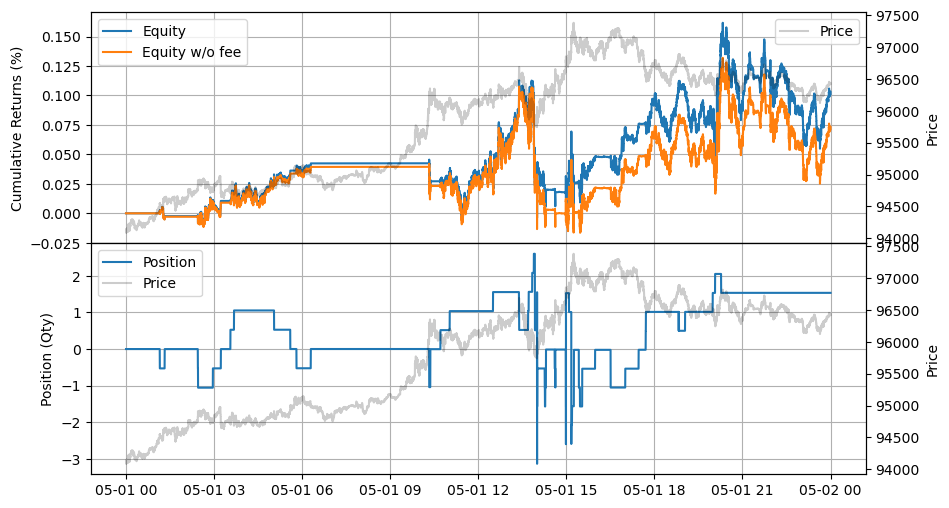

Backtesting with Fused Data

[22]:

data = recorder.get(0)

stats = (

LinearAssetRecord(data)

.resample('1s')

.stats(book_size=1_000_000)

)

stats.summary()

[22]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2025-05-01 00:00:00 | 2025-05-01 23:59:59 | 10.345893 | 14.320701 | 0.001011 | 0.001167 | 119.001377 | 5.950202 | 0.865768 | 0.00017 | 301079.3632 |

[23]:

stats.plot()

[23]:

You may notice slight differences in order fills, which lead to position discrepancies and, ultimately, equity differences — particularly between 03:00 and 15:00. These order fill differences are closely tied to the order placement behavior, which depends on the characteristics of the strategy. The differences in the BBO as shown above can result in significant equity divergence during backtesting.

Note: Some tutorial—especially older ones—were not backtested with fused market depth.

Wrapping up

Since it uses more frequent data feeds, the backtesting process takes longer. There is always a trade-off between accuracy and speed in backtesting—there is no one-size-fits-all solution. Relaxing certain conditions, such as order queue position and latency modeling, can significantly speed up the process. Not all strategies require precise modeling of these factors, especially when dealing with small tick sizes and highly volatile assets like BTCUSDT. Please see the next tutorial about accelerated backtesting.