Market Making with Alpha - APT

Overview

Continuing from Market Making with Alpha - Basis, this example demonstrates market making based on Arbitrage Pricing Theory.

Note: This example is for educational purposes only and demonstrates effective strategies for high-frequency market-making schemes. All backtests are based on a 0.005% rebate, the highest market maker rebate available on Binance Futures. See Binance Upgrades USDⓢ-Margined Futures Liquidity Provider Program for more details.

[1]:

import datetime

import os

import numpy as np

from numba import njit, uint64

from numba.typed import Dict

from hftbacktest import (

BacktestAsset,

ROIVectorMarketDepthBacktest,

GTX,

LIMIT,

BUY,

SELL,

BUY_EVENT,

SELL_EVENT,

Recorder

)

from hftbacktest.stats import LinearAssetRecord

import polars as pl

import statsmodels.api as sm

from matplotlib import pyplot

def load_bookticker(file):

return pl.read_csv(file, schema={

'exchange': pl.String,

'symbol': pl.String,

'timestamp': pl.Int64,

'local_timestamp': pl.Int64,

'ask_amount': pl.Float64,

'ask_price': pl.Float64,

'bid_price': pl.Float64,

'bid_amount': pl.Float64

}).with_columns(

pl.col('local_timestamp').cast(pl.Datetime),

mid_price = (.5 * (pl.col('bid_price') + pl.col('ask_price'))),

).select(['local_timestamp', 'mid_price'])

def prepare_px_return(spot_file, futures_file, sampling_interval, rolling_window, shift):

spot = load_bookticker(spot_file)

futures = load_bookticker(futures_file)

# Resamples prices to calculate returns.

spot_rs = spot.group_by_dynamic(

index_column='local_timestamp',

every=sampling_interval

).agg(

pl.col('mid_price').last()

).upsample(

time_column='local_timestamp',

every=sampling_interval

).select(pl.all().forward_fill())

futures_rs = futures.group_by_dynamic(

index_column='local_timestamp',

every=sampling_interval

).agg(

pl.col('mid_price').last(),

).upsample(

time_column='local_timestamp',

every=sampling_interval

).select(pl.all().forward_fill())

# When computing returns, if one chooses the past price at a specific time point,

# it may result in selecting an noiser value, leading to a noisier return calculation.

#

# To mitigate this issue, the average price over a past period is used.

# For example, to compute 5-minute returns, the average price over a 5-minute window centered around 5 minutes ago is used.

return spot_rs.join(

futures_rs,

left_on='local_timestamp',

right_on='local_timestamp',

how='full'

).with_columns(

futures_px=pl.col('mid_price_right').forward_fill(),

spot_px=pl.col('mid_price').forward_fill()

).with_columns(

futures_past_px=pl.col('futures_px').rolling_mean(window_size=rolling_window).shift(shift),

spot_past_px=pl.col('spot_px').rolling_mean(window_size=rolling_window).shift(shift)

).with_columns(

local_timestamp=pl.col('local_timestamp').dt.timestamp('ns'),

spot_return=pl.col('spot_px') / pl.col('spot_past_px') - 1,

futures_return=pl.col('futures_px') / pl.col('futures_past_px') - 1,

).select(

['local_timestamp', 'spot_return', 'spot_past_px', 'futures_return', 'futures_past_px']

)

[2]:

start_date = datetime.datetime.strptime('20240901', '%Y%m%d')

end_date = datetime.datetime.strptime('20241031', '%Y%m%d')

[3]:

data = []

date = start_date

while date <= end_date:

data.append(prepare_px_return(

f'spot/book_ticker/BTCUSDT/BTCUSDT_{date.strftime("%Y%m%d")}.csv.gz',

f'usdm/book_ticker/BTCUSDT/BTCUSDT_{date.strftime("%Y%m%d")}.csv.gz',

'100ms',

3000, # 5-minute

1500 # 2.5-minute, the average price over a 5-minute window centered around 5 minutes ago

).to_numpy())

date += datetime.timedelta(days=1)

precompute_data = np.concatenate(data, axis=0)

[4]:

np.savez_compressed("precompute_px_return_BTCUSDT_5m", data=precompute_data)

[5]:

precompute_data = np.load("precompute_px_return_BTCUSDT_5m.npz")["data"]

[6]:

spot_returns = precompute_data[:, 1]

futures_returns = precompute_data[:, 3]

m = np.isfinite(spot_returns) & np.isfinite(futures_returns)

spot_returns = spot_returns[m]

futures_returns = futures_returns[m]

[7]:

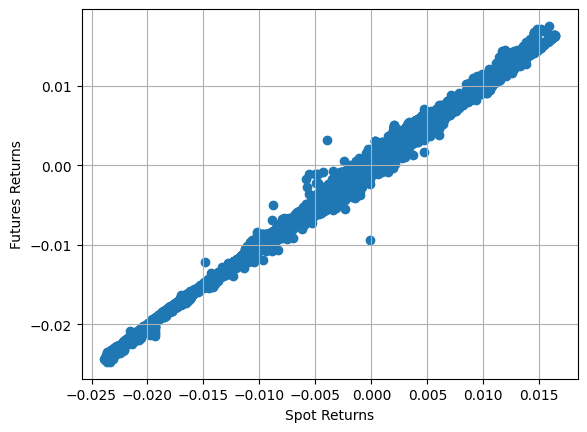

pyplot.scatter(spot_returns, futures_returns)

pyplot.xlabel('Spot Returns')

pyplot.ylabel('Futures Returns')

pyplot.grid()

Under Arbitrage Pricing Theory, the relationship between futures return and spot return can be expressed as:

\(Return_{futures} = \alpha + \beta_{spot} * Return_{spot}\)

Under the assumption that \(\beta_{spot}\) = 1 and \(\alpha\) = 0, the futures return should be equal to the spot return. This also implies that any residual movement is mean-reverting to zero, similar to what is shown in the basis example.

Extending the Model

Beyond this basic relationship, additional return-contributing factors can be incorporated. For instance, returns from other exchanges’ Bitcoin markets, such as:

CME Bitcoin futures, Bybit’s BTC futures and other platforms’s BTC futures

Bitcoin ETFs

Spot prices from Coinbase, Kraken, and other platforms

Moreover, this is not limited to the same asset. Other cryptocurrencies, traditional assets, and macroeconomic indices can be considered, such as:

Ethereum (ETH)

S&P 500

Dollar Index

Additionally, market microstructure factors, such as order book imbalance, can further enhance the model, as demonstrated in our other example.

This broader framework allows for a more comprehensive understanding of price movements and their underlying drivers.

[10]:

@njit

def apt_mm(

hbt,

stat,

half_spread,

skew,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval_,

roi_lb,

roi_ub

):

asset_no = 0

tick_size = hbt.depth(0).tick_size

lot_size = hbt.depth(0).lot_size

roi_lb_tick = int(round(roi_lb / tick_size))

roi_ub_tick = int(round(roi_ub / tick_size))

data_i = 0

spot_return = np.nan

futures_past_px = np.nan

while hbt.elapse(interval) == 0:

hbt.clear_inactive_orders(asset_no)

depth = hbt.depth(asset_no)

position = hbt.position(asset_no)

orders = hbt.orders(asset_no)

best_bid = depth.best_bid

best_ask = depth.best_ask

while data_i < len(precompute_data):

if precompute_data[data_i, 0] > hbt.current_timestamp:

if data_i > 0:

spot_return = precompute_data[data_i - 1, 1]

futures_past_px = precompute_data[data_i - 1, 4]

break

data_i += 1

#--------------------------------------------------------

# Computes bid price and ask price.

mid_price = (best_bid + best_ask) / 2.0

order_qty = max(round((order_qty_dollar / mid_price) / lot_size) * lot_size, lot_size)

normalized_position = position / order_qty

relative_bid_depth = half_spread + skew * normalized_position

relative_ask_depth = half_spread - skew * normalized_position

beta = 1

alpha = 0

return_ = beta * spot_return + alpha

fair_px = (1 + return_) * futures_past_px

bid_price = min(fair_px * (1.0 - relative_bid_depth), best_bid)

ask_price = max(fair_px * (1.0 + relative_ask_depth), best_ask)

bid_price = np.floor(bid_price / tick_size) * tick_size

ask_price = np.ceil(ask_price / tick_size) * tick_size

grid_interval = max(tick_size, np.round(grid_interval_ * fair_px / tick_size) * tick_size)

# Aligns the prices to the grid.

bid_price = np.floor(bid_price / grid_interval) * grid_interval

ask_price = np.ceil(ask_price / grid_interval) * grid_interval

#--------------------------------------------------------

# Updates quotes.

# Creates a new grid for buy orders.

new_bid_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price < max_position_dollar and np.isfinite(bid_price):

for i in range(grid_num):

bid_price_tick = round(bid_price / tick_size)

# order price in tick is used as order id.

new_bid_orders[uint64(bid_price_tick)] = bid_price

bid_price -= grid_interval

# Creates a new grid for sell orders.

new_ask_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price > -max_position_dollar and np.isfinite(ask_price):

for i in range(grid_num):

ask_price_tick = round(ask_price / tick_size)

# order price in tick is used as order id.

new_ask_orders[uint64(ask_price_tick)] = ask_price

ask_price += grid_interval

order_values = orders.values();

while order_values.has_next():

order = order_values.get()

# Cancels if a working order is not in the new grid.

if order.cancellable:

if (

(order.side == BUY and order.order_id not in new_bid_orders)

or (order.side == SELL and order.order_id not in new_ask_orders)

):

hbt.cancel(asset_no, order.order_id, False)

for order_id, order_price in new_bid_orders.items():

# Posts a new buy order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_buy_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

for order_id, order_price in new_ask_orders.items():

# Posts a new sell order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_sell_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

# Records the current state for stat calculation.

stat.record(hbt)

[11]:

%%time

roi_lb = 10000

roi_ub = 90000

latency_data = []

date = start_date

while date <= end_date:

latency_data.append('latency/order_latency_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

data = []

date = start_date

while date <= end_date:

data.append('data2/btcusdt_{}.npz'.format(date.strftime("%Y%m%d")))

date += datetime.timedelta(days=1)

asset = (

BacktestAsset()

.data(data)

.initial_snapshot('data2/btcusdt_20240831_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

half_spread = 0.0003 # a ratio relative to the fair price

skew = half_spread / 20

interval = 100_000_000 # in nanoseconds. 100ms

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 20

grid_num = 1

grid_interval = hbt.depth(0).tick_size

apt_mm(

hbt,

recorder.recorder,

half_spread,

skew,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/underlying_btcusdt_return_5m.npz')

CPU times: user 1h 2min 18s, sys: 1min 45s, total: 1h 4min 3s

Wall time: 40min 2s

[12]:

data = np.load('stats/underlying_btcusdt_return_5m.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

The history saving thread hit an unexpected error (OperationalError('database is locked')).History will not be written to the database.

[12]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2024-09-01 00:00:00 | 2024-10-31 23:55:00 | 3.578158 | 4.821155 | 0.025127 | 0.010283 | 568.442193 | 11.368845 | 2.443528 | 0.000036 | 1.0415e6 |

[13]:

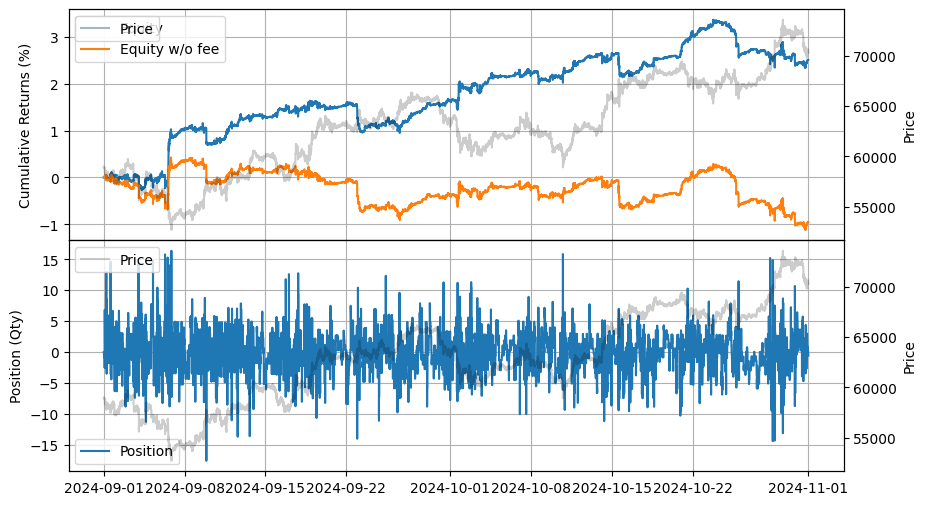

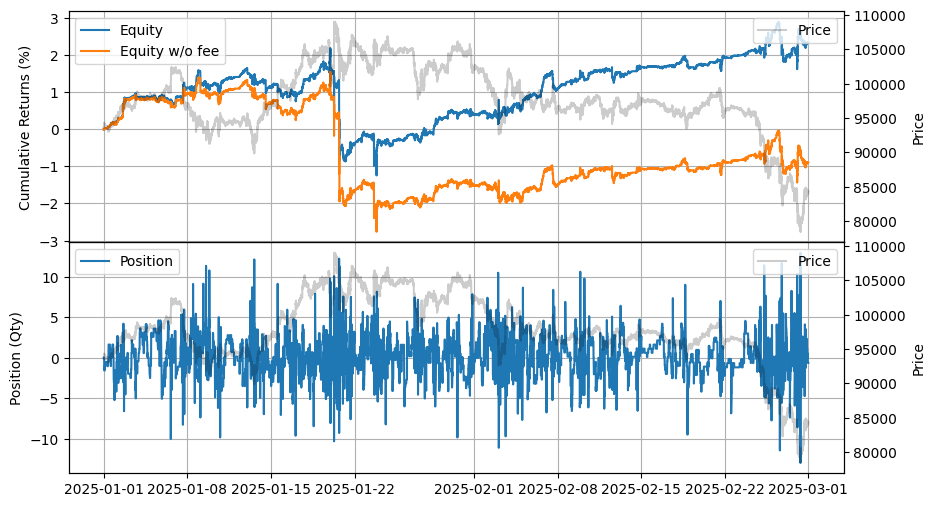

stats.plot()

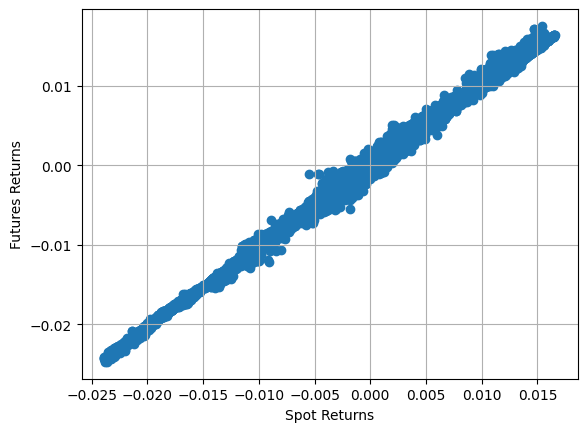

As demonstrated in the basis example, BTCFDUSD behaves in a similar manner.

[15]:

data = []

date = start_date

while date <= end_date:

data.append(prepare_px_return(

f'spot/book_ticker/BTCFDUSD/BTCFDUSD_{date.strftime("%Y%m%d")}.csv.gz',

f'usdm/book_ticker/BTCUSDT/BTCUSDT_{date.strftime("%Y%m%d")}.csv.gz',

'100ms',

3000, # 5-minute window

1500 # 2.5-minute, the average price over a 5-minute window centered around 5 minutes ago

).to_numpy())

date += datetime.timedelta(days=1)

precompute_data = np.concatenate(data, axis=0)

[16]:

np.savez_compressed("precompute_px_return_BTCFDUSD_5m", data=precompute_data)

[17]:

precompute_data = np.load("precompute_px_return_BTCFDUSD_5m.npz")["data"]

[18]:

spot_returns = precompute_data[:, 1]

futures_returns = precompute_data[:, 3]

m = np.isfinite(spot_returns) & np.isfinite(futures_returns)

spot_returns = spot_returns[m]

futures_returns = futures_returns[m]

[19]:

pyplot.scatter(spot_returns, futures_returns)

pyplot.xlabel('Spot Returns')

pyplot.ylabel('Futures Returns')

pyplot.grid()

[21]:

%%time

roi_lb = 10000

roi_ub = 90000

latency_data = []

date = start_date

while date <= end_date:

latency_data.append('latency/order_latency_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

data = []

date = start_date

while date <= end_date:

data.append('data2/btcusdt_{}.npz'.format(date.strftime("%Y%m%d")))

date += datetime.timedelta(days=1)

asset = (

BacktestAsset()

.data(data)

.initial_snapshot('data2/btcusdt_20240831_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

half_spread = 0.0003 # a ratio relative to the fair price

skew = half_spread / 20

interval = 100_000_000 # in nanoseconds. 100ms

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 20

grid_num = 1

grid_interval = hbt.depth(0).tick_size

apt_mm(

hbt,

recorder.recorder,

half_spread,

skew,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/underlying_btcfdusd_return_5m.npz')

CPU times: user 1h 4min 56s, sys: 1min 52s, total: 1h 6min 48s

Wall time: 42min 35s

[22]:

data = np.load('stats/underlying_btcfdusd_return_5m.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

[22]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2024-09-01 00:00:00 | 2024-10-31 23:55:00 | 3.125613 | 4.000555 | 0.031671 | 0.020096 | 504.372972 | 10.087474 | 1.575961 | 0.000051 | 1.2871e6 |

[23]:

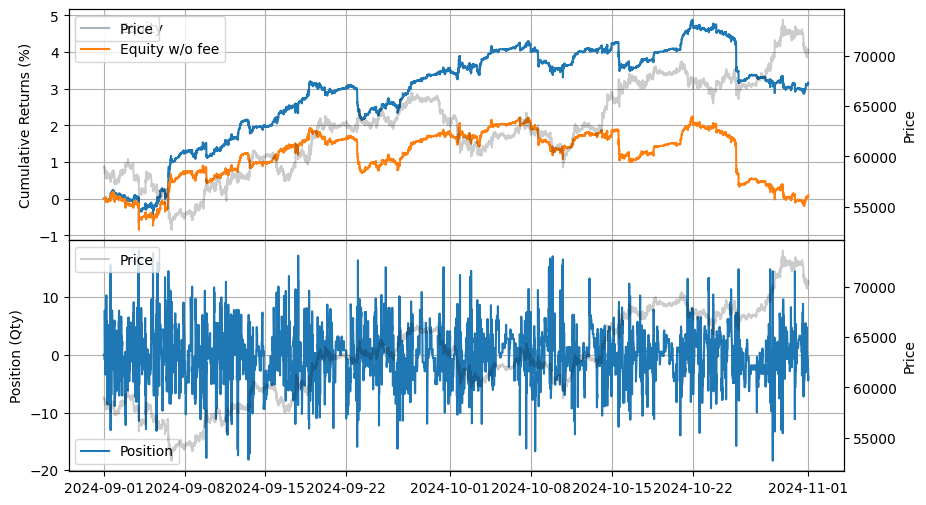

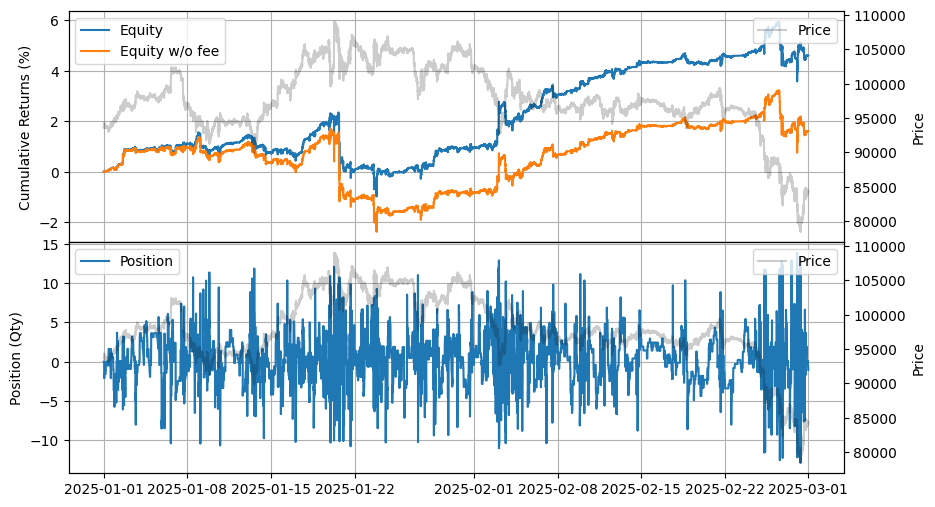

stats.plot()

Integrating Grid Trading

[25]:

start_date = datetime.datetime.strptime('20250101', '%Y%m%d')

end_date = datetime.datetime.strptime('20250228', '%Y%m%d')

[26]:

data = []

date = start_date

while date <= end_date:

data.append(prepare_px_return(

f'spot/book_ticker/BTCUSDT/BTCUSDT_{date.strftime("%Y%m%d")}.csv.gz',

f'usdm/book_ticker/BTCUSDT/BTCUSDT_{date.strftime("%Y%m%d")}.csv.gz',

'100ms',

3000, # 5-minute

1500 # 2.5-minute, the average price over a 5-minute window centered around 5 minutes ago

).to_numpy())

date += datetime.timedelta(days=1)

precompute_data = np.concatenate(data, axis=0)

[27]:

np.savez_compressed("precompute_px_return_BTCUSDT_5m_2025", data=precompute_data)

[28]:

precompute_data = np.load("precompute_px_return_BTCUSDT_5m_2025.npz")["data"]

[29]:

%%time

roi_lb = 50000

roi_ub = 150000

latency_data = []

date = start_date

while date <= end_date:

latency_data.append('latency/order_latency_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

data = []

date = start_date

while date <= end_date:

data.append('data2/btcusdt_{}.npz'.format(date.strftime("%Y%m%d")))

date += datetime.timedelta(days=1)

asset = (

BacktestAsset()

.data(data)

.initial_snapshot('data2/btcusdt_20241231_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

half_spread = 0.0003 # a ratio relative to the fair price

skew = half_spread / 20

interval = 100_000_000 # in nanoseconds. 100ms

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 20

grid_num = 5

grid_interval = 0.0003 # a ratio relative to the fair price

apt_mm(

hbt,

recorder.recorder,

half_spread,

skew,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/underlying_btcusdt_return_5m_2025.npz')

CPU times: user 1h 31min 28s, sys: 2min 50s, total: 1h 34min 18s

Wall time: 59min 57s

[30]:

data = np.load('stats/underlying_btcusdt_return_5m_2025.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

[30]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2025-01-01 00:00:00 | 2025-02-28 23:55:00 | 1.509583 | 1.891524 | 0.023263 | 0.034334 | 546.794891 | 10.935656 | 0.677544 | 0.000036 | 1.2789e6 |

[31]:

stats.plot()

[32]:

data = []

date = start_date

while date <= end_date:

data.append(prepare_px_return(

f'spot/book_ticker/BTCFDUSD/BTCFDUSD_{date.strftime("%Y%m%d")}.csv.gz',

f'usdm/book_ticker/BTCUSDT/BTCUSDT_{date.strftime("%Y%m%d")}.csv.gz',

'100ms',

3000, # 5-minute

1500 # 2.5-minute, the average price over a 5-minute window centered around 5 minutes ago

).to_numpy())

date += datetime.timedelta(days=1)

precompute_data = np.concatenate(data, axis=0)

[33]:

np.savez_compressed("precompute_px_return_BTCFDUSD_5m_202502", data=precompute_data)

[34]:

precompute_data = np.load('precompute_px_return_BTCFDUSD_5m_2025.npz')['data']

[35]:

%%time

roi_lb = 50000

roi_ub = 150000

latency_data = []

date = start_date

while date <= end_date:

latency_data.append('latency/order_latency_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

data = []

date = start_date

while date <= end_date:

data.append('data2/btcusdt_{}.npz'.format(date.strftime("%Y%m%d")))

date += datetime.timedelta(days=1)

asset = (

BacktestAsset()

.data(data)

.initial_snapshot('data2/btcusdt_20241231_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

half_spread = 0.0003 # a ratio relative to the fair price

skew = half_spread / 20

interval = 100_000_000 # in nanoseconds. 100ms

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 20

grid_num = 5

grid_interval = 0.0003 # a ratio relative to the fair price

apt_mm(

hbt,

recorder.recorder,

half_spread,

skew,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/underlying_btcfdusd_return_5m_202502.npz')

CPU times: user 1h 31min 38s, sys: 2min 56s, total: 1h 34min 34s

Wall time: 1h 8s

[36]:

data = np.load('stats/underlying_btcfdusd_return_5m_202502.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

[36]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2025-01-01 00:00:00 | 2025-02-28 23:55:00 | 2.43417 | 3.17886 | 0.045953 | 0.033234 | 506.877288 | 10.137426 | 1.382702 | 0.000077 | 1.3039e6 |

[37]:

stats.plot()

Extension to the Multi-Factor Model

Simple Form: Utilizing Both BTCUSDT and BTCFDUSD Spot Returns

One of the simplest ways to incorporate both BTCUSDT and BTCFDUSD spot returns is by using equal beta, which takes the average of these two values.

[39]:

precompute_data1 = np.load('precompute_px_return_BTCUSDT_5m_2025.npz')['data']

precompute_data2 = np.load('precompute_px_return_BTCFDUSD_5m_2025.npz')['data']

[40]:

df1 = pl.DataFrame(precompute_data1).filter(

pl.col('column_0').is_not_nan()

).with_columns(

pl.col('column_0').cast(pl.Int64),

)

df2 = pl.DataFrame(precompute_data2).filter(

pl.col('column_0').is_not_nan()

).with_columns(

pl.col('column_0').cast(pl.Int64),

)

[41]:

precompute_data = df1.join(

df2,

left_on='column_0',

right_on='column_0',

how='full'

).sort(

'column_0'

).filter(

pl.col('column_0').is_not_null()

).select(

local_timestamp = 'column_0',

btcusdt_spot_return = 'column_1',

btcfdusd_spot_return = 'column_1_right',

futures_past_px = 'column_4',

futures_return = 'column_3'

).to_numpy()

[42]:

@njit

def apt_multi_mm(

hbt,

stat,

half_spread,

skew,

beta,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval_,

roi_lb,

roi_ub

):

asset_no = 0

tick_size = hbt.depth(0).tick_size

lot_size = hbt.depth(0).lot_size

roi_lb_tick = int(round(roi_lb / tick_size))

roi_ub_tick = int(round(roi_ub / tick_size))

data_i = 0

spot_return = np.nan

futures_past_px = np.nan

while hbt.elapse(interval) == 0:

hbt.clear_inactive_orders(asset_no)

depth = hbt.depth(asset_no)

position = hbt.position(asset_no)

orders = hbt.orders(asset_no)

best_bid = depth.best_bid

best_ask = depth.best_ask

while data_i < len(precompute_data):

if precompute_data[data_i, 0] > hbt.current_timestamp:

if data_i > 0:

spot1_return = precompute_data[data_i - 1, 1]

spot2_return = precompute_data[data_i - 1, 2]

futures_past_px = precompute_data[data_i - 1, 3]

break

data_i += 1

#--------------------------------------------------------

# Computes bid price and ask price.

mid_price = (best_bid + best_ask) / 2.0

order_qty = max(round((order_qty_dollar / mid_price) / lot_size) * lot_size, lot_size)

normalized_position = position / order_qty

relative_bid_depth = half_spread + skew * normalized_position

relative_ask_depth = half_spread - skew * normalized_position

alpha = 0

return_ = beta[0] * spot1_return + beta[1] * spot2_return + alpha

fair_px = (1 + return_) * futures_past_px

bid_price = min(fair_px * (1.0 - relative_bid_depth), best_bid)

ask_price = max(fair_px * (1.0 + relative_ask_depth), best_ask)

bid_price = np.floor(bid_price / tick_size) * tick_size

ask_price = np.ceil(ask_price / tick_size) * tick_size

grid_interval = max(tick_size, np.round(grid_interval_ * fair_px / tick_size) * tick_size)

# Aligns the prices to the grid.

bid_price = np.floor(bid_price / grid_interval) * grid_interval

ask_price = np.ceil(ask_price / grid_interval) * grid_interval

#--------------------------------------------------------

# Updates quotes.

# Creates a new grid for buy orders.

new_bid_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price < max_position_dollar and np.isfinite(bid_price):

for i in range(grid_num):

bid_price_tick = round(bid_price / tick_size)

# order price in tick is used as order id.

new_bid_orders[uint64(bid_price_tick)] = bid_price

bid_price -= grid_interval

# Creates a new grid for sell orders.

new_ask_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price > -max_position_dollar and np.isfinite(ask_price):

for i in range(grid_num):

ask_price_tick = round(ask_price / tick_size)

# order price in tick is used as order id.

new_ask_orders[uint64(ask_price_tick)] = ask_price

ask_price += grid_interval

order_values = orders.values();

while order_values.has_next():

order = order_values.get()

# Cancels if a working order is not in the new grid.

if order.cancellable:

if (

(order.side == BUY and order.order_id not in new_bid_orders)

or (order.side == SELL and order.order_id not in new_ask_orders)

):

hbt.cancel(asset_no, order.order_id, False)

for order_id, order_price in new_bid_orders.items():

# Posts a new buy order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_buy_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

for order_id, order_price in new_ask_orders.items():

# Posts a new sell order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_sell_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

# Records the current state for stat calculation.

stat.record(hbt)

[43]:

%%time

roi_lb = 50000

roi_ub = 150000

latency_data = []

date = start_date

while date <= end_date:

latency_data.append('latency/order_latency_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

data = []

date = start_date

while date <= end_date:

data.append('data2/btcusdt_{}.npz'.format(date.strftime("%Y%m%d")))

date += datetime.timedelta(days=1)

asset = (

BacktestAsset()

.data(data)

.initial_snapshot('data2/btcusdt_20241231_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

half_spread = 0.0003 # a ratio relative to the fair price

skew = half_spread / 20

interval = 100_000_000 # in nanoseconds. 100ms

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 20

grid_num = 5

grid_interval = 0.0003 # a ratio relative to the fair price

beta = np.asarray([0.5, 0.5])

apt_multi_mm(

hbt,

recorder.recorder,

half_spread,

skew,

beta,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/underlying_btcspot_return_5m_2025.npz')

CPU times: user 1h 33min 2s, sys: 3min, total: 1h 36min 2s

Wall time: 1h 1min 31s

[44]:

data = np.load('stats/underlying_btcspot_return_5m_2025.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

[44]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2025-01-01 00:00:00 | 2025-02-28 23:55:00 | 2.266827 | 2.920951 | 0.038573 | 0.03424 | 489.961038 | 9.799065 | 1.126546 | 0.000067 | 1.3342e6 |

[45]:

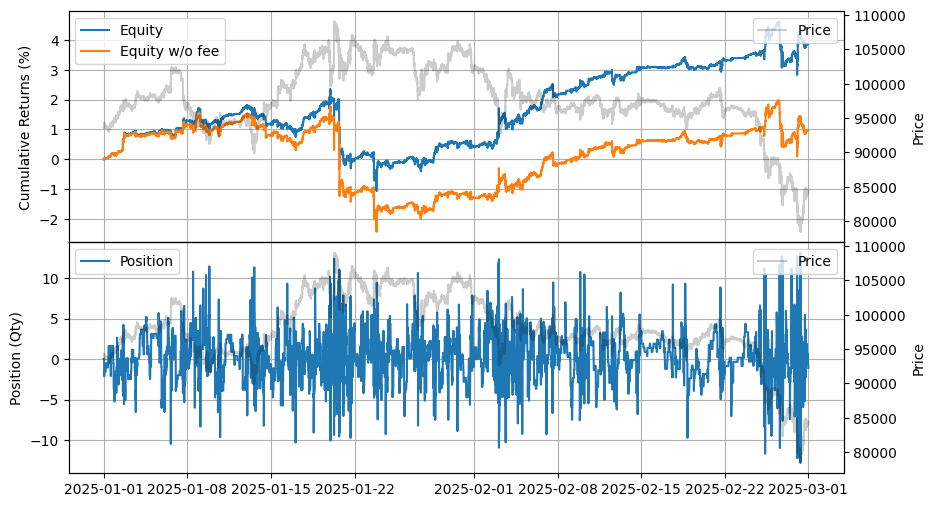

stats.plot()

MLR: Utilizing Both BTCUSDT and BTCFDUSD Spot Returns

Since these two variables are highly correlated, proper handling is necessary. One approach is the residual method, but other techniques, such as PCA, can also be used to eliminate correlation. Additionally, when applying Multiple Linear Regression, you may need to constrain beta values within a specific range, such as ensuring they remain positive. In such cases, more advanced techniques can be utilized.

[47]:

ts = datetime.datetime(2025, 2, 1, tzinfo=datetime.timezone.utc).timestamp() * 1_000_000_000

train_end = np.min(np.where(df['local_timestamp'] > ts))

[48]:

precompute_data = df.filter(

pl.col('btcusdt_spot_return').is_not_nan()

& pl.col('btcfdusd_spot_return').is_not_nan()

& pl.col('futures_return').is_not_nan()

).to_numpy()

Given the assumption that the deviation in futures returns mean-reverts to the spot return, the target is set as the spot return.

[49]:

# Regresses BTCUSDT spot returns on BTCFDUSD spot returns to get residuals.

# x1 = BTCFDUSD spot returns

# x2 = BTCUSDT spot returns

x1 = sm.add_constant(precompute_data[:train_end, 2])

model_x2 = sm.OLS(precompute_data[:train_end, 1], x1).fit()

x2_residual = precompute_data[:train_end, 2] - model_x2.predict(x1)

# Regresses BTCUSDT futures returns on BTCFDUSD spot returns and the residual of BTCUSDT spot returns.

X = sm.add_constant(np.column_stack((precompute_data[:train_end, 2], x2_residual)))

model = sm.OLS(precompute_data[:train_end, 4], X).fit()

print(model.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.997

Model: OLS Adj. R-squared: 0.997

Method: Least Squares F-statistic: 9.707e+09

Date: Sun, 09 Mar 2025 Prob (F-statistic): 0.00

Time: 10:52:52 Log-Likelihood: 2.1219e+08

No. Observations: 26644398 AIC: -4.244e+08

Df Residuals: 26644396 BIC: -4.244e+08

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -2.297e-07 1.63e-08 -14.084 0.000 -2.62e-07 -1.98e-07

x1 1.0164 1.03e-05 9.85e+04 0.000 1.016 1.016

x2 -0.0117 1.19e-07 -9.85e+04 0.000 -0.012 -0.012

==============================================================================

Omnibus: 31540719.034 Durbin-Watson: 0.091

Prob(Omnibus): 0.000 Jarque-Bera (JB): 594213867106.353

Skew: -4.722 Prob(JB): 0.00

Kurtosis: 734.540 Cond. No. 1.12e+19

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The smallest eigenvalue is 2.13e-31. This might indicate that there are

strong multicollinearity problems or that the design matrix is singular.

[50]:

%%time

roi_lb = 50000

roi_ub = 150000

latency_data = []

date = start_date

while date <= end_date:

latency_data.append('latency/order_latency_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

data = []

date = start_date

while date <= end_date:

data.append('data2/btcusdt_{}.npz'.format(date.strftime("%Y%m%d")))

date += datetime.timedelta(days=1)

asset = (

BacktestAsset()

.data(data)

.initial_snapshot('data2/btcusdt_20241231_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

half_spread = 0.0003 # a ratio relative to the fair price

skew = half_spread / 20

interval = 100_000_000 # in nanoseconds. 100ms

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 20

grid_num = 5

grid_interval = 0.0003 # a ratio relative to the fair price

beta = np.asarray([-0.0117, 1.0164])

apt_multi_mm(

hbt,

recorder.recorder,

half_spread,

skew,

beta,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/underlying_btcspot2_return_5m_2025.npz')

CPU times: user 1h 29min 31s, sys: 3min 11s, total: 1h 32min 42s

Wall time: 58min 22s

[51]:

data = np.load('stats/underlying_btcspot2_return_5m_2025.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=2_500_000)

)

stats.summary()

[51]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2025-01-01 00:00:00 | 2025-02-28 23:55:00 | 3.066696 | 4.017417 | 0.057006 | 0.030539 | 533.455123 | 10.66894 | 1.86669 | 0.000091 | 1.3075e6 |

[52]:

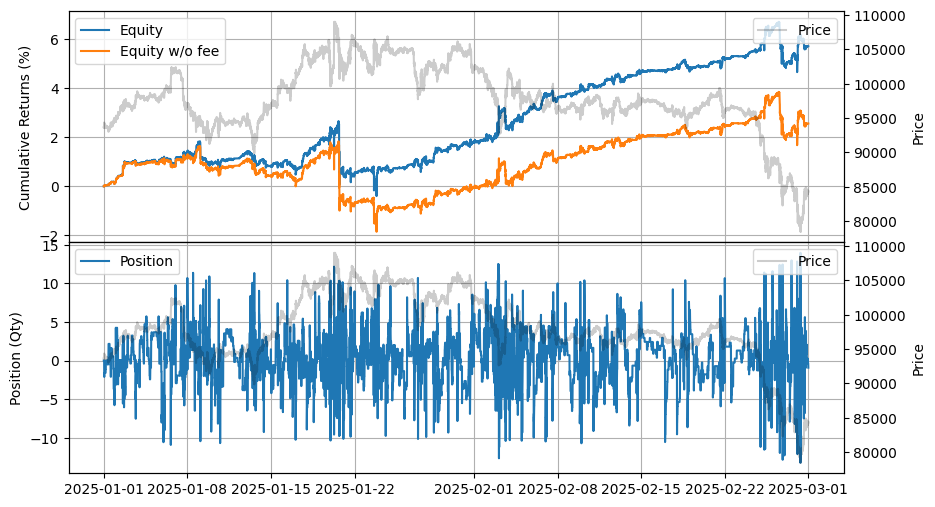

stats.plot()

A Comprehensive Framework for Pricing Models

Let’s explore a more generalized approach to asset pricing from a conceptual standpoint.

Core Market Drivers (Primary Price Movement)

The first component represents price movement driven by core market instruments — typically spot and futures markets across major venues. It can be expressed as:

Return_BTC = β00 * BTCUSDT_spot

+ β01 * BTCFDUSD_spot

+ β02 * BTCUSDT_futures_on_exchange1

+ β03 * BTCUSD_inverse_perpetual1

+ β04 * BTCUSD_CME_futures

+ β05 * BTC_ETF1

+ ...

This model doesn’t require all components. You can identify the most influential inputs using statistical methods (e.g., regression, PCA, or Granger causality), or by analyzing market depth, trading volume, and lead-lag relationships between exchanges. You can also see the importance of considering the Trad-Fi market — including CME futures, Bitcoin ETFs, and equity markets — by comparing weekday returns, which highlight a different return profile on weekends (typically better).

Broader Market Influence (Cross-Asset Correlation)

Bitcoin’s price can also be influenced by the movement of other major cryptocurrencies — similar to how components interact with an index:

Return_CrossAsset = β10 * ETHUSDT_futures

+ β11 * SOLUSDT_futures

+ ...

You may also use spot markets, but it’s important to select markets with high liquidity and trading volume, as they are more likely to drive broader price movements.

Microstructure Signals & Alpha Factors

Short-term price forecasts can benefit from market microstructure data and proprietary alpha signals. These might include:

Return_Alpha = β20 * OrderBookImbalance1

+ β21 * OrderBookImbalance2

+ β22 * FundingRateAlpha

+ β23 * OpenInterestAlpha

+ ...

+ β2n * CustomAlpha_n

These signals are especially valuable for short-horizon trading, such as high-frequency or latency-sensitive strategies.

Combined Pricing Model

All components can be integrated into a single predictive return model:

Forecast_Return = β0 * Return_Self

+ Return_BTC

+ Return_CrossAsset

+ Return_Alpha

Return_BTC and Return_CrossAsset reflect structural or market-level influences and Return_Alpha represents short-term, predictive signals based on microstructure or custom models. In addition, defining fair value price is crucial, as it shapes your trading setup. A straight defintion is to forecast future returns (e.g., 10s, 30s, 1min, 5min), depending on the trading horizon. The regression target should then be this fair value price.

Exchange-Specific Application

The effectiveness of this model may depend on your forecasting horizon:

For medium-term forecasts (e.g., 1–5 minutes), this model can generalize across major venues such as Binance, Bybit, OKX, and Hyperliquid.

For very short-term trading (e.g., sub-second to a few seconds), you need to account for exchange-specific dynamics such as latency, liquidity, and order flow patterns.

For example, since Binance Futures has the highest trading volume, its price movements often lead the market. Other exchanges may lag behind.

The simplest cross-exchange model might look like this:

Return_Bybit ≈ Return_Binance

This setup is useful for cross-exchange arbitrage or liquidity-driven strategies, where you exploit short-term dislocations between platforms.

More examples incorporating additional factors beyond BTC returns and cross-exchange cases such as described in https://hangukquant.github.io/scripts/market_making, will be added.