Market Making with Alpha - Basis

Note: This example is for educational purposes only and demonstrates effective strategies for high-frequency market-making schemes. All backtests are based on a 0.005% rebate, the highest market maker rebate available on Binance Futures. See Binance Upgrades USDⓢ-Margined Futures Liquidity Provider Program for more details.

[1]:

import datetime

import os

import numpy as np

from numba import njit, uint64

from numba.typed import Dict

from hftbacktest import (

BacktestAsset,

ROIVectorMarketDepthBacktest,

GTX,

LIMIT,

BUY,

SELL,

BUY_EVENT,

SELL_EVENT,

Recorder

)

from hftbacktest.stats import LinearAssetRecord

import polars as pl

Download L1 (book ticker) data to calculate the basis between spot and futures.

[3]:

start_date = datetime.datetime.strptime('20240901', '%Y%m%d')

end_date = datetime.datetime.strptime('20241031', '%Y%m%d')

tardis_token = ""

[4]:

def download_from_tardis(exchange, stream, symbol, start_date, end_date, output_path, token):

date = start_date

while date <= end_date:

yyyymmdd = date.strftime('%Y%m%d')

year = yyyymmdd[:4]

month = yyyymmdd[4:6]

day = yyyymmdd[6:]

output_file = os.path.join(output_path, f'{symbol}_{yyyymmdd}.csv.gz')

header = f'"Authorization: Bearer {token}"'

!wget --header={header} https://datasets.tardis.dev/v1/{exchange}/{stream}/{year}/{month}/{day}/{symbol}.csv.gz -O {output_file}

date += datetime.timedelta(days=1)

[5]:

download_from_tardis('binance', 'book_ticker', 'BTCUSDT', start_date, end_date, 'spot/book_ticker/BTCUSDT', tardis_token)

download_from_tardis('binance-futures', 'book_ticker', 'BTCUSDT', start_date, end_date, 'usdm/book_ticker/BTCUSDT', tardis_token)

Precompute the basis for faster backtesting.

[7]:

def load_bookticker(file):

return pl.read_csv(file, schema={

'exchange': pl.String,

'symbol': pl.String,

'timestamp': pl.Int64,

'local_timestamp': pl.Int64,

'ask_amount': pl.Float64,

'ask_price': pl.Float64,

'bid_price': pl.Float64,

'bid_amount': pl.Float64

}).with_columns(

pl.col('local_timestamp').cast(pl.Datetime),

mid_price = (.5 * (pl.col('bid_price') + pl.col('ask_price'))),

).select(['local_timestamp', 'mid_price'])

def prepare_px_basis(spot_file, futures_file, sampling_interval, rolling_window):

spot = load_bookticker(spot_file)

futures = load_bookticker(futures_file)

# Resamples prices to calculate the basis.

spot_rs = spot.group_by_dynamic(

index_column='local_timestamp',

every=sampling_interval

).agg(

pl.col('mid_price').last()

).upsample(

time_column='local_timestamp',

every=sampling_interval

).select(pl.all().forward_fill())

futures_rs = futures.group_by_dynamic(

index_column='local_timestamp',

every=sampling_interval

).agg(

pl.col('mid_price').last(),

).upsample(

time_column='local_timestamp',

every=sampling_interval

).select(pl.all().forward_fill())

return spot_rs.join(

futures_rs,

left_on='local_timestamp',

right_on='local_timestamp',

how='full'

).with_columns(

rolling_mean_basis=(

pl.col('mid_price_right').forward_fill() - pl.col('mid_price').forward_fill() # Computes the basis

).rolling_mean(window_size=rolling_window), # Computes the moving average of the basis over the given window.

).select(

local_timestamp=pl.col('local_timestamp').dt.timestamp('ns'),

spot=pl.col('mid_price'),

basis=pl.col('rolling_mean_basis')

)

[8]:

data = []

date = start_date

while date <= end_date:

data.append(prepare_px_basis(

f'spot/book_ticker/BTCUSDT/BTCUSDT_{date.strftime("%Y%m%d")}.csv.gz',

f'usdm/book_ticker/BTCUSDT/BTCUSDT_{date.strftime("%Y%m%d")}.csv.gz',

'100ms',

3000 # 5-minute

).to_numpy())

date += datetime.timedelta(days=1)

precompute_data = np.concatenate(data, axis=0)

[9]:

np.savez_compressed('px_basis_BTCUSDT_5m', data=precompute_data)

[10]:

precompute_data = np.load('px_basis_BTCUSDT_5m.npz')['data']

A market-making model based on the basis. Since the basis is often considered stationary, various time series analysis techniques, such as MA, AR, ARMA and etc, can be applied. Here, the simplest model, the Moving Average, is used for demonstration. This approach assumes that the basis will revert to the average of a given past period.

[12]:

@njit

def basis_mm(

hbt,

stat,

half_spread,

skew,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

):

asset_no = 0

tick_size = hbt.depth(0).tick_size

lot_size = hbt.depth(0).lot_size

roi_lb_tick = int(round(roi_lb / tick_size))

roi_ub_tick = int(round(roi_ub / tick_size))

data_i = 0

last_spot = np.nan

last_basis = np.nan

while hbt.elapse(interval) == 0:

hbt.clear_inactive_orders(asset_no)

depth = hbt.depth(asset_no)

position = hbt.position(asset_no)

orders = hbt.orders(asset_no)

best_bid = depth.best_bid

best_ask = depth.best_ask

mid_price = (best_bid + best_ask) / 2.0

#--------------------------------------------------------

# Computes bid price and ask price.

order_qty = max(round((order_qty_dollar / mid_price) / lot_size) * lot_size, lot_size)

normalized_position = position / order_qty

relative_bid_depth = half_spread + skew * normalized_position

relative_ask_depth = half_spread - skew * normalized_position

# Reads the latest observable spot price and basis from the precomputed data.

while data_i < len(precompute_data):

if precompute_data[data_i, 0] > hbt.current_timestamp:

if data_i > 0:

last_spot = precompute_data[data_i - 1, 1]

last_basis = precompute_data[data_i - 1, 2]

break

data_i += 1

# Our fair price is calculated as the spot price + the rolling average of the basis

fair_px = last_spot + last_basis

bid_price = min(fair_px * (1.0 - relative_bid_depth), best_bid)

ask_price = max(fair_px * (1.0 + relative_ask_depth), best_ask)

bid_price = np.floor(bid_price / tick_size) * tick_size

ask_price = np.ceil(ask_price / tick_size) * tick_size

#--------------------------------------------------------

# Updates quotes.

# Creates a new grid for buy orders.

new_bid_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price < max_position_dollar and np.isfinite(bid_price):

for i in range(grid_num):

bid_price_tick = round(bid_price / tick_size)

# order price in tick is used as order id.

new_bid_orders[uint64(bid_price_tick)] = bid_price

bid_price -= grid_interval

# Creates a new grid for sell orders.

new_ask_orders = Dict.empty(np.uint64, np.float64)

if position * mid_price > -max_position_dollar and np.isfinite(ask_price):

for i in range(grid_num):

ask_price_tick = round(ask_price / tick_size)

# order price in tick is used as order id.

new_ask_orders[uint64(ask_price_tick)] = ask_price

ask_price += grid_interval

order_values = orders.values();

while order_values.has_next():

order = order_values.get()

# Cancels if a working order is not in the new grid.

if order.cancellable:

if (

(order.side == BUY and order.order_id not in new_bid_orders)

or (order.side == SELL and order.order_id not in new_ask_orders)

):

hbt.cancel(asset_no, order.order_id, False)

for order_id, order_price in new_bid_orders.items():

# Posts a new buy order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_buy_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

for order_id, order_price in new_ask_orders.items():

# Posts a new sell order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_sell_order(asset_no, order_id, order_price, order_qty, GTX, LIMIT, False)

# Records the current state for stat calculation.

stat.record(hbt)

[13]:

%%time

roi_lb = 10000

roi_ub = 90000

latency_data = []

date = start_date

while date <= end_date:

latency_data.append('latency/order_latency_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

data = []

date = start_date

while date <= end_date:

data.append('data2/btcusdt_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

asset = (

BacktestAsset()

.data(data)

.initial_snapshot('data2/btcusdt_20240831_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

half_spread = 0.0003 # a ratio relative to the fair price

skew = half_spread / 20

interval = 100_000_000 # in nanoseconds. 100ms

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 20

grid_num = 1

grid_interval = hbt.depth(0).tick_size

basis_mm(

hbt,

recorder.recorder,

half_spread,

skew,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/underlying_btcusdt_basis_5m.npz')

CPU times: user 1h 2min 41s, sys: 1min 45s, total: 1h 4min 27s

Wall time: 40min 22s

[14]:

data = np.load('stats/underlying_btcusdt_basis_5m.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=1_000_000)

)

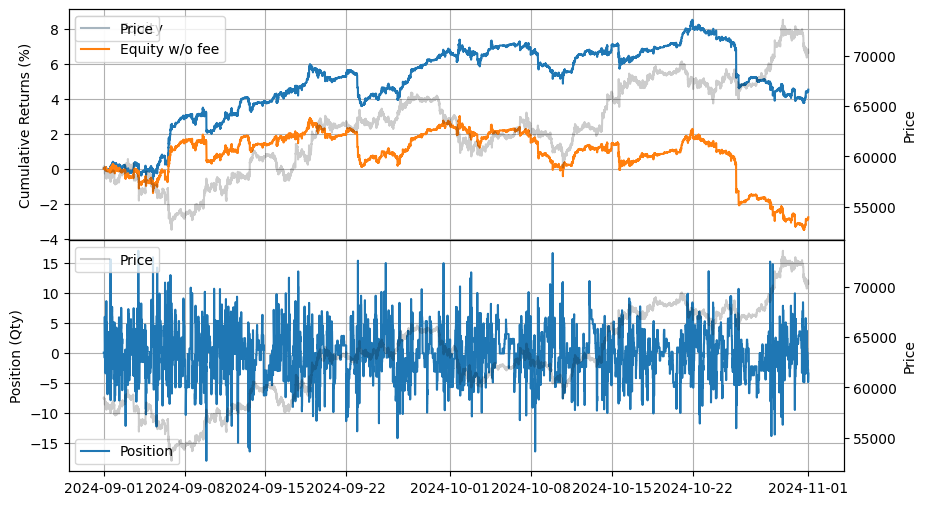

stats.summary()

[14]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2024-09-01 00:00:00 | 2024-10-31 23:55:00 | 3.280936 | 4.380048 | 0.05166 | 0.024406 | 537.702738 | 26.885072 | 2.116701 | 0.000032 | 1.0409e6 |

[15]:

stats.plot()

On Binance, the BTCFDUSD spot market has a higher trading volume than the BTCUSDT spot market. BTCFDUSD records a daily trading volume of \$3 billion, while BTCUSDT has \$2.5 billion. Alternatively, you may consider using the exact index rather than a specific spot.

You can find the weights composing the index using the API. https://developers.binance.com/docs/derivatives/usds-margined-futures/market-data/rest-api/Composite-Index-Symbol-Information

[17]:

download_from_tardis('binance', 'book_ticker', 'BTCFDUSD', start_date, end_date, 'spot/book_ticker/BTCFDUSD', tardis_token)

[18]:

data = []

date = start_date

while date <= end_date:

data.append(prepare_px_basis(

f'spot/book_ticker/BTCFDUSD/BTCFDUSD_{date.strftime("%Y%m%d")}.csv.gz',

f'usdm/book_ticker/BTCUSDT/BTCUSDT_{date.strftime("%Y%m%d")}.csv.gz',

'100ms',

3000 # 5-minute

).to_numpy())

date += datetime.timedelta(days=1)

precompute_data = np.concatenate(data, axis=0)

[19]:

np.savez_compressed('px_basis_BTCFDUSD_5m', data=precompute_data)

[20]:

precompute_data = np.load('px_basis_BTCFDUSD_5m.npz')['data']

[21]:

%%time

roi_lb = 10000

roi_ub = 90000

latency_data = []

date = start_date

while date <= end_date:

latency_data.append('latency/order_latency_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

data = []

date = start_date

while date <= end_date:

data.append('data2/btcusdt_{}.npz'.format(date.strftime('%Y%m%d')))

date += datetime.timedelta(days=1)

asset = (

BacktestAsset()

.data(data)

.initial_snapshot('data2/btcusdt_20240831_eod.npz')

.linear_asset(1.0)

.intp_order_latency(latency_data)

.power_prob_queue_model(3)

.no_partial_fill_exchange()

.trading_value_fee_model(-0.00005, 0.0007)

.tick_size(0.1)

.lot_size(0.001)

.roi_lb(roi_lb)

.roi_ub(roi_ub)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 60_000_000)

half_spread = 0.0003 # a ratio relative to the fair price

skew = half_spread / 20

interval = 100_000_000 # in nanoseconds. 100ms

order_qty_dollar = 50_000

max_position_dollar = order_qty_dollar * 20

grid_num = 1

grid_interval = hbt.depth(0).tick_size

basis_mm(

hbt,

recorder.recorder,

half_spread,

skew,

precompute_data,

interval,

order_qty_dollar,

max_position_dollar,

grid_num,

grid_interval,

roi_lb,

roi_ub

)

hbt.close()

recorder.to_npz('stats/underlying_btcfdusd_basis_5m.npz')

CPU times: user 1h 5min 24s, sys: 1min 50s, total: 1h 7min 14s

Wall time: 42min 59s

[22]:

data = np.load('stats/underlying_btcfdusd_basis_5m.npz')['0']

stats = (

LinearAssetRecord(data)

.resample('5m')

.stats(book_size=1_000_000)

)

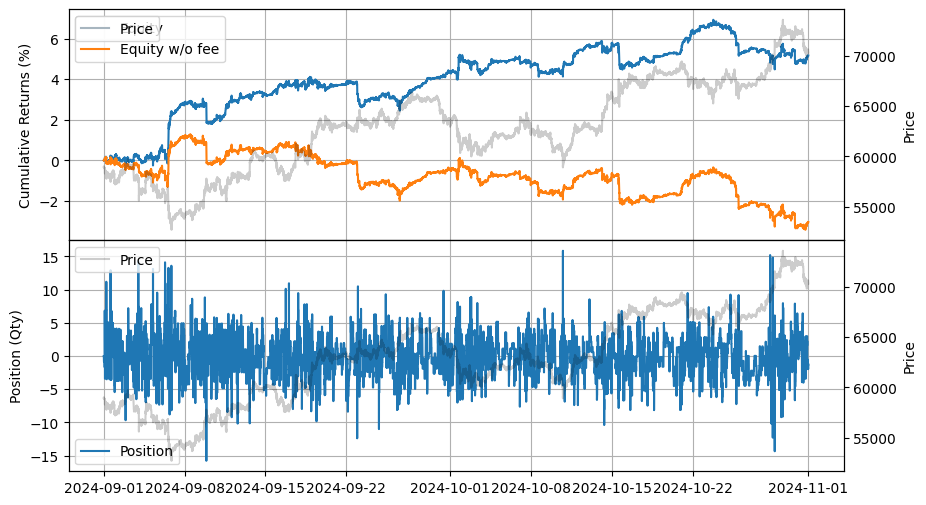

stats.summary()

[22]:

| start | end | SR | Sortino | Return | MaxDrawdown | DailyNumberOfTrades | DailyTurnover | ReturnOverMDD | ReturnOverTrade | MaxPositionValue |

|---|---|---|---|---|---|---|---|---|---|---|

| datetime[μs] | datetime[μs] | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 2024-09-01 00:00:00 | 2024-10-31 23:55:00 | 2.069684 | 2.647596 | 0.045228 | 0.047641 | 479.043661 | 23.952189 | 0.949337 | 0.000031 | 1.0376e6 |

[23]:

stats.plot()