Level-3 Backtesting

The Level-3 feed data for HftBacktest is built from DataBento’s CME Market-By-Order data

[1]:

from hftbacktest.data.utils import databento

for date in range(20240609, 20240615):

databento.convert(f'data/db/glbx-mdp3-{date}.mbo.dbn.zst', 'BTCM4', output_filename=f'data/BTCM4_{date}_l3.npz')

Correcting the latency

Correcting the event order

Saving to data/BTCM4_20240609_l3.npz

Correcting the latency

Correcting the event order

Saving to data/BTCM4_20240610_l3.npz

Correcting the latency

Correcting the event order

Saving to data/BTCM4_20240611_l3.npz

Correcting the latency

Correcting the event order

Saving to data/BTCM4_20240612_l3.npz

Correcting the latency

Correcting the event order

Saving to data/BTCM4_20240613_l3.npz

Correcting the latency

Correcting the event order

Saving to data/BTCM4_20240614_l3.npz

[2]:

import numpy as np

from numba import njit, uint64, float64

from numba.typed import Dict

from hftbacktest import BUY, SELL, GTC, LIMIT

@njit

def gridtrading(hbt, recorder, skew):

asset_no = 0

tick_size = hbt.depth(asset_no).tick_size

grid_num = 10

max_position = 5

grid_interval = tick_size * 1

half_spread = tick_size * 0.4

# Running interval in nanoseconds.

while hbt.elapse(100_000_000) == 0:

# Clears cancelled, filled or expired orders.

hbt.clear_inactive_orders(asset_no)

depth = hbt.depth(asset_no)

position = hbt.position(asset_no)

orders = hbt.orders(asset_no)

best_bid = depth.best_bid

best_ask = depth.best_ask

mid_price = (best_bid + best_ask) / 2.0

order_qty = 1 # np.round(notional_order_qty / mid_price / hbt.depth(asset_no).lot_size) * hbt.depth(asset_no).lot_size

# The personalized price that considers skewing based on inventory risk is introduced,

# which is described in the well-known Stokov-Avalleneda market-making paper.

# https://math.nyu.edu/~avellane/HighFrequencyTrading.pdf

alpha = 0

reservation_price = mid_price + alpha - skew * tick_size * position

# Since our price is skewed, it may cross the spread. To ensure market making and avoid crossing the spread,

# limit the price to the best bid and best ask.

bid_price = np.minimum(reservation_price - half_spread, best_bid)

ask_price = np.maximum(reservation_price + half_spread, best_ask)

# Aligns the prices to the grid.

bid_price = np.floor(bid_price / grid_interval) * grid_interval

ask_price = np.ceil(ask_price / grid_interval) * grid_interval

#--------------------------------------------------------

# Updates quotes.

# Creates a new grid for buy orders.

new_bid_orders = Dict.empty(np.uint64, np.float64)

if position < max_position and np.isfinite(bid_price): # position * mid_price < max_notional_position

for i in range(grid_num):

bid_price_tick = round(bid_price / tick_size)

# order price in tick is used as order id.

new_bid_orders[uint64(bid_price_tick)] = bid_price

bid_price -= grid_interval

# Creates a new grid for sell orders.

new_ask_orders = Dict.empty(np.uint64, np.float64)

if position > -max_position and np.isfinite(ask_price): # position * mid_price > -max_notional_position

for i in range(grid_num):

ask_price_tick = round(ask_price / tick_size)

# order price in tick is used as order id.

new_ask_orders[uint64(ask_price_tick)] = ask_price

ask_price += grid_interval

order_values = orders.values();

while order_values.has_next():

order = order_values.get()

# Cancels if a working order is not in the new grid.

if order.cancellable:

if (

(order.side == BUY and order.order_id not in new_bid_orders)

or (order.side == SELL and order.order_id not in new_ask_orders)

):

hbt.cancel(asset_no, order.order_id, False)

for order_id, order_price in new_bid_orders.items():

# Posts a new buy order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_buy_order(asset_no, order_id, order_price, order_qty, GTC, LIMIT, False)

for order_id, order_price in new_ask_orders.items():

# Posts a new sell order if there is no working order at the price on the new grid.

if order_id not in orders:

hbt.submit_sell_order(asset_no, order_id, order_price, order_qty, GTC, LIMIT, False)

# Records the current state for stat calculation.

recorder.record(hbt)

return True

[3]:

from hftbacktest import BacktestAsset, ROIVectorMarketDepthBacktest, Recorder

asset = (

BacktestAsset()

.data([

'data/BTCM4_20240609_l3.npz',

'data/BTCM4_20240610_l3.npz',

'data/BTCM4_20240611_l3.npz',

'data/BTCM4_20240612_l3.npz',

'data/BTCM4_20240613_l3.npz',

'data/BTCM4_20240614_l3.npz',

])

.linear_asset(5)

.constant_latency(100_000, 100_000)

.l3_fifo_queue_model()

.no_partial_fill_exchange()

.trading_qty_fee_model(5, 5)

.tick_size(5)

.lot_size(1)

.roi_lb(0.0)

.roi_ub(100000.0)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 5_000_0000)

[4]:

%%time

gridtrading(hbt, recorder.recorder, 0.5)

_ = hbt.close()

CPU times: user 35.6 s, sys: 336 ms, total: 35.9 s

Wall time: 32.4 s

[5]:

from hftbacktest.stats import LinearAssetRecord

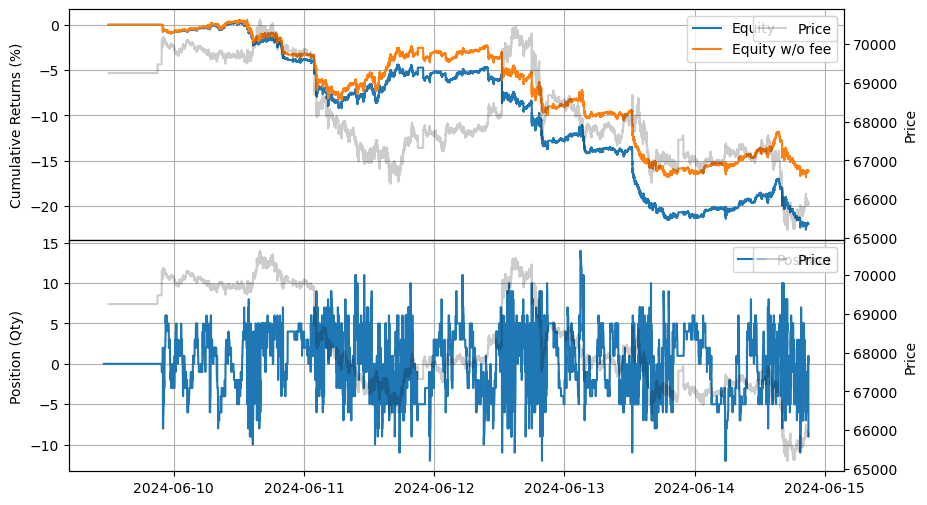

stats = LinearAssetRecord(recorder.get(0)).contract_size(5).stats(book_size=1_000_000)

l3_backtest_equity = stats.entire['equity_wo_fee']

stats.plot()

The following code constructs Level-2 data from Level-3 data for the purpose of comparing backtesting results between Level-3 and Level-2. Level-2 estimates queue positions using a model, whereas Level-3 determines queue positions directly from the order data.

[6]:

from hftbacktest.data import correct_event_order, validate_event_order

from hftbacktest import (

EXCH_EVENT,

LOCAL_EVENT,

TRADE_EVENT,

DEPTH_EVENT,

DEPTH_CLEAR_EVENT,

ADD_ORDER_EVENT,

MODIFY_ORDER_EVENT,

CANCEL_ORDER_EVENT,

FILL_EVENT,

BUY_EVENT,

SELL_EVENT,

event_dtype

)

from numba.experimental import jitclass

from numba.types import DictType, int64

@jitclass

class L3MarketDepth:

bid_depth: DictType(int64, float64)

ask_depth: DictType(int64, float64)

order_book_px: DictType(uint64, float64)

order_book_qty: DictType(uint64, float64)

tick_size: float64

def __init__(self, tick_size):

self.bid_depth = Dict.empty(int64, float64)

self.ask_depth = Dict.empty(int64, float64)

self.order_book_px = Dict.empty(uint64, float64)

self.order_book_qty = Dict.empty(uint64, float64)

self.tick_size = tick_size

def add_order(self, ev):

if ev.order_id in self.order_book_qty:

print('add_order: OrderIdExist', ev.order_id)

raise ValueError

self.order_book_px[ev.order_id] = ev.px;

l2_ev = np.empty(1, event_dtype)

l2_ev[0] = ev

l2_ev[0].ev = (l2_ev[0].ev & ~0xff) | DEPTH_EVENT

price_tick = int(round(ev.px / self.tick_size))

if ev.ev & BUY_EVENT == BUY_EVENT:

self.order_book_qty[ev.order_id] = ev.qty;

if price_tick not in self.bid_depth:

self.bid_depth[price_tick] = 0.0

self.bid_depth[price_tick] += ev.qty

l2_ev[0].qty = round(self.bid_depth[price_tick])

elif ev.ev & SELL_EVENT == SELL_EVENT:

self.order_book_qty[ev.order_id] = -ev.qty;

if price_tick not in self.ask_depth:

self.ask_depth[price_tick] = 0.0

self.ask_depth[price_tick] += ev.qty

l2_ev[0].qty = round(self.ask_depth[price_tick])

return l2_ev[0]

def modify_order(self, ev):

if ev.order_id not in self.order_book_qty:

print('modify_order: OrderNotFound', ev.order_id)

raise ValueError

prev_px = self.order_book_px[ev.order_id]

prev_qty = self.order_book_qty[ev.order_id]

l2_ev = np.empty(2, event_dtype)

l2_ev[1] = l2_ev[0] = ev

l2_ev[0].ev = (l2_ev[0].ev & ~0xff) | DEPTH_EVENT

n = 0

if prev_qty > 0:

price_tick = int(round(prev_px / self.tick_size))

self.bid_depth[price_tick] -= prev_qty

if int(round(prev_px / self.tick_size)) != int(round(ev.px / self.tick_size)):

l2_ev[0].px = prev_px

l2_ev[0].qty = round(self.bid_depth[price_tick])

n = 1

elif prev_qty < 0:

price_tick = int(round(prev_px / self.tick_size))

self.ask_depth[price_tick] -= np.abs(prev_qty)

if int(round(prev_px / self.tick_size)) != int(round(ev.px / self.tick_size)):

l2_ev[0].px = prev_px

l2_ev[0].qty = round(self.ask_depth[price_tick])

n = 1

self.order_book_px[ev.order_id] = ev.px;

price_tick = int(round(ev.px / self.tick_size))

if ev.ev & BUY_EVENT == BUY_EVENT:

self.order_book_qty[ev.order_id] = ev.qty;

if price_tick not in self.bid_depth:

self.bid_depth[price_tick] = 0.0

self.bid_depth[price_tick] += ev.qty

l2_ev[n].qty = round(self.bid_depth[price_tick])

elif ev.ev & SELL_EVENT == SELL_EVENT:

self.order_book_qty[ev.order_id] = -ev.qty;

if price_tick not in self.ask_depth:

self.ask_depth[price_tick] = 0.0

self.ask_depth[price_tick] += ev.qty

l2_ev[n].qty = round(self.ask_depth[price_tick])

return l2_ev[:n + 1]

def cancel_order(self, ev):

if ev.order_id not in self.order_book_qty:

print('cancel_order: OrderNotFound', ev.order_id, ev)

raise ValueError

del self.order_book_px[ev.order_id]

del self.order_book_qty[ev.order_id]

l2_ev = np.empty(1, event_dtype)

l2_ev[0] = ev

l2_ev[0].ev = (l2_ev[0].ev & ~0xff) | DEPTH_EVENT

if ev.ev & BUY_EVENT == BUY_EVENT:

price_tick = int(round(ev.px / self.tick_size))

self.bid_depth[price_tick] -= ev.qty

l2_ev[0].qty = round(self.bid_depth[price_tick])

elif ev.ev & SELL_EVENT == SELL_EVENT:

price_tick = int(round(ev.px / self.tick_size))

self.ask_depth[price_tick] -= ev.qty

l2_ev[0].qty = round(self.ask_depth[price_tick])

return l2_ev[0]

def clear(self):

self.order_book_px.clear()

self.order_book_qty.clear()

self.bid_depth.clear()

self.ask_depth.clear()

@njit

def convert_l3_to_l2(data, tick_size):

result = np.empty(len(data) * 4, event_dtype)

local_md = L3MarketDepth(tick_size)

exch_md = L3MarketDepth(tick_size)

rn = 0

for i in range(len(data)):

if data[i].ev & (EXCH_EVENT | LOCAL_EVENT) == EXCH_EVENT | LOCAL_EVENT:

if data[i].ev & 0xff == ADD_ORDER_EVENT:

result[rn] = exch_md.add_order(data[i])

rn += 1

elif data[i].ev & 0xff == MODIFY_ORDER_EVENT:

l2_ev = exch_md.modify_order(data[i])

result[rn] = l2_ev[0]

rn += 1

if len(l2_ev) == 2:

result[rn] = l2_ev[1]

rn += 1

elif data[i].ev & 0xff == CANCEL_ORDER_EVENT:

result[rn] = exch_md.cancel_order(data[i])

rn += 1

elif data[i].ev & 0xff == FILL_EVENT:

continue

elif data[i].ev & 0xff == DEPTH_CLEAR_EVENT:

exch_md.clear()

result[rn] = data[i]

rn += 1

else:

result[rn] = data[i]

rn += 1

else:

# DataBento's CME data is aligned in both local and exchange timestamps.

raise ValueError

return result[:rn]

[7]:

for date in range(20240609, 20240615):

l3 = databento.convert(f'data/db/glbx-mdp3-{date}.mbo.dbn.zst', 'BTCM4')

tick_size = 5

l2 = convert_l3_to_l2(l3, tick_size)

data = correct_event_order(

l2,

np.argsort(l2['exch_ts'], kind='mergesort'),

np.argsort(l2['local_ts'], kind='mergesort')

)

validate_event_order(data)

np.savez_compressed(f'data/BTCM4_{date}_l2.npz', data=data)

Correcting the latency

Correcting the event order

Correcting the latency

Correcting the event order

Correcting the latency

Correcting the event order

Correcting the latency

Correcting the event order

Correcting the latency

Correcting the event order

Correcting the latency

Correcting the event order

[8]:

from hftbacktest import BacktestAsset, ROIVectorMarketDepthBacktest, Recorder

asset = (

BacktestAsset()

.data([

'data/BTCM4_20240609_l2.npz',

'data/BTCM4_20240610_l2.npz',

'data/BTCM4_20240611_l2.npz',

'data/BTCM4_20240612_l2.npz',

'data/BTCM4_20240613_l2.npz',

'data/BTCM4_20240614_l2.npz',

])

.linear_asset(5)

.constant_latency(100_000, 100_000)

.power_prob_queue_model3(3.0)

.no_partial_fill_exchange()

.trading_qty_fee_model(5, 5)

.tick_size(5)

.lot_size(1)

.roi_lb(0.0)

.roi_ub(100000.0)

)

hbt = ROIVectorMarketDepthBacktest([asset])

recorder = Recorder(1, 5_000_0000)

[9]:

%%time

gridtrading(hbt, recorder.recorder, 0.5)

_ = hbt.close()

CPU times: user 28.9 s, sys: 401 ms, total: 29.3 s

Wall time: 24.9 s

[10]:

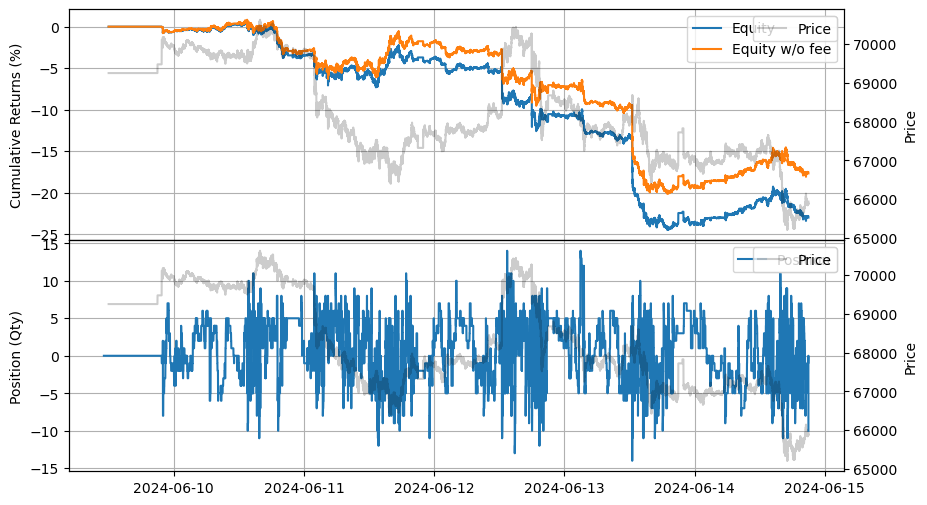

stats = LinearAssetRecord(recorder.get(0)).contract_size(5).stats(book_size=1_000_000)

l2_backtest_equity = stats.entire['equity_wo_fee']

stats.plot()

[11]:

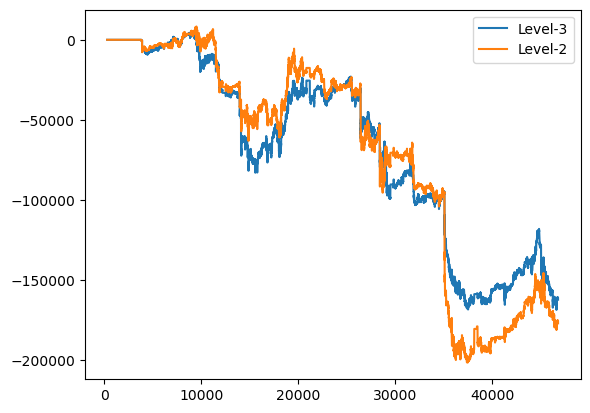

from matplotlib import pyplot as plt

plt.plot(l3_backtest_equity)

plt.plot(l2_backtest_equity)

plt.legend(['Level-3', 'Level-2'])

[11]:

<matplotlib.legend.Legend at 0x7f58f9b4ac20>

The impact of the difference can vary depending on the characteristics of the strategy; for some strategies, Level-2 estimation may be sufficiently accurate, while for others, it may not be. This comparison is intended to highlight these differences. In markets that only provide Level-2 data, it is important to develop a realistic queue position model based on live trading data. Although Level-3 data offers direct order queue position information, it is still crucial to validate backtesting results against live trading results. For example, in this CME Level-3 backtest, the market depth doesn’t include implied orders.